Published: 11/07/2023 By Mateo Asminian & Katherine McDowall

Sales Review Q2 2023By Mateo Asminian — Sales, Andrew Nunn & Associates

Quarter 2, a traditionally busy time post Easter and embracing the Spring market, started strongly with upbeat demand taking out the new Spring instructions, but with these beginning to dry up and buyer motivation dropping as a result, we are entering the summer on a more cautious note. Inflation and interest rates are key here. At the start of the quarter, the cost of fixed-rate mortgage money appeared to have peaked (and indeed was falling), which gave house hunters confidence to go out and buy; however, inflation hasn’t fallen back as expected and, hence, on the 22nd of June we saw the thirteenth consecutive interest rate rise. Consequently, the cost of fixed rate mortgages is rising once again.

|

|

|

|

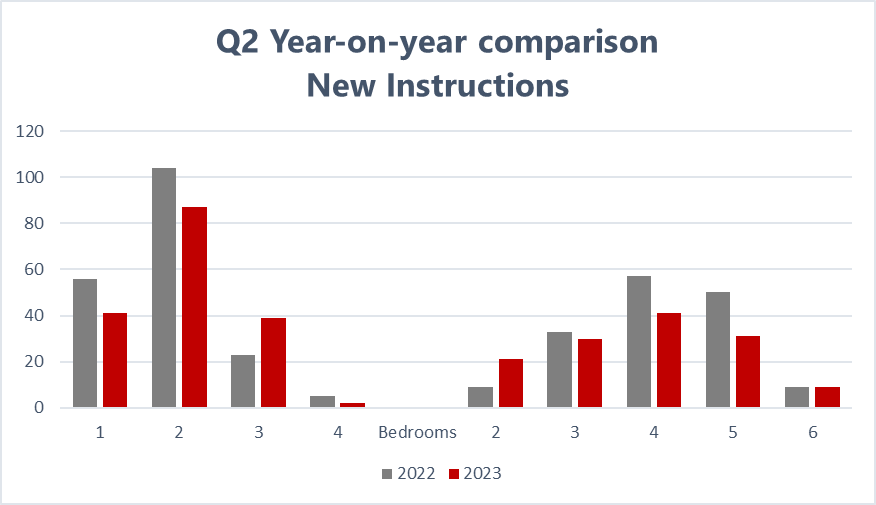

Instructions

Our independently collated data shows that the total volume of new properties coming onto the market has slipped when comparing to the same period in 2022 as the sentiment continues to shift from the buzz of last year.

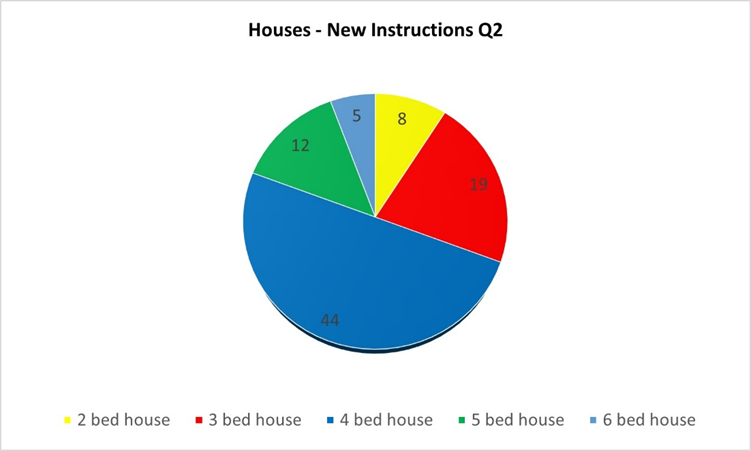

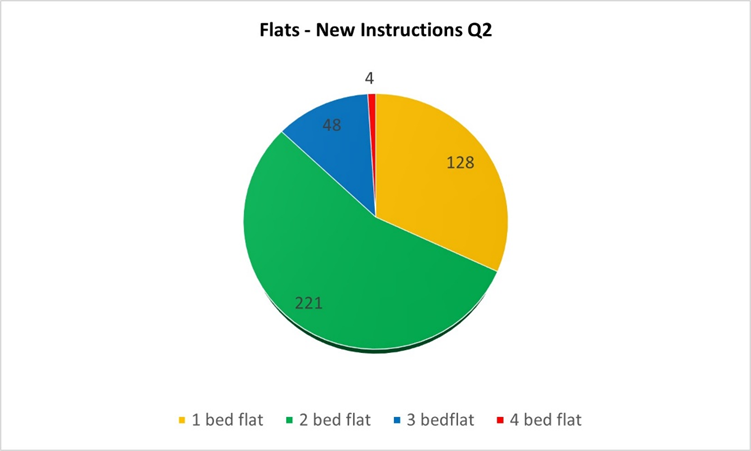

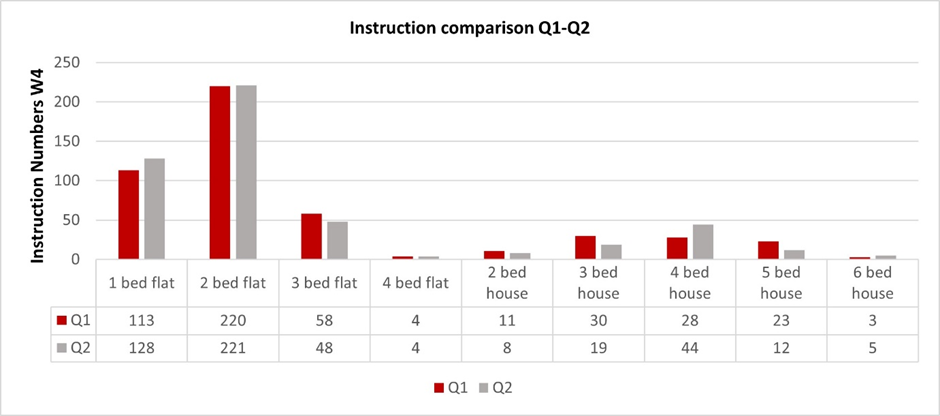

It is no secret that W4’s excellent schooling, amenities and transport links make it an extremely popular area for families in search of a ‘forever’ homes – and, as we often tell buyers, “when they’re gone, they’re gone”… typically, for decades. Through these long periods of repayments and organic capital growth, house owners are more likely to have built sizeable equity in their properties, providing a cushion during turbulent economic times and meaning that fewer houses sold are ‘forced’ sales.Furthermore, we are undoubtedly now feeling the domino effect of the spike in activity of the last couple of years, with many families having brought their moves forward, or finally realised them after the uncertainty of Covid-19 had neutralised and with reports suggesting it was a good time to sell. As a result of these two factors, those searching for houses in Q2 of this year had 12% fewer options to choose from than Q2 of 2022. Instructions for flats also showed a deficit when comparing to last year, this time of 14%, as we see offices continue to encourage workplace working, making switching a flat for an affordable house further away from the city less appealing.

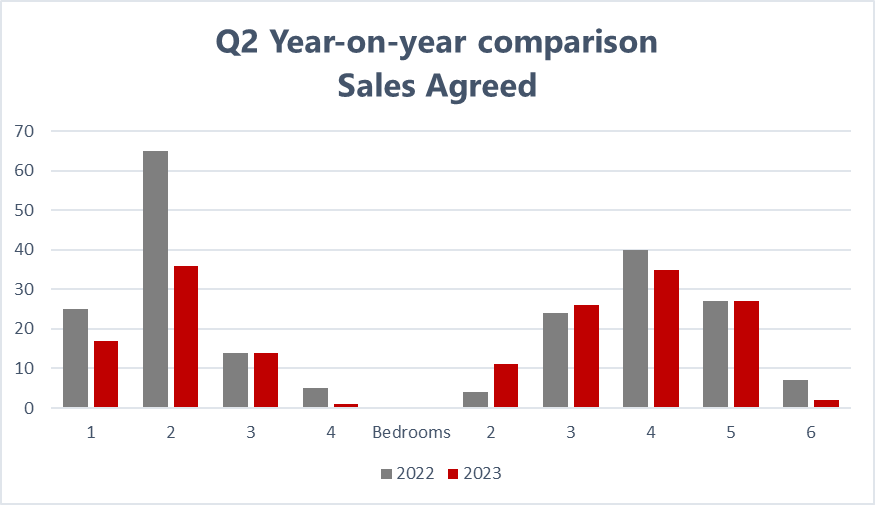

Sales Agreed

While new flat and house instructions have slowed at a similar rate, their sales numbers paint a slightly different picture. Long term family homes were most sought after in Q2 as clever money poured into bricks and mortar to serve as an inflationary hedge.

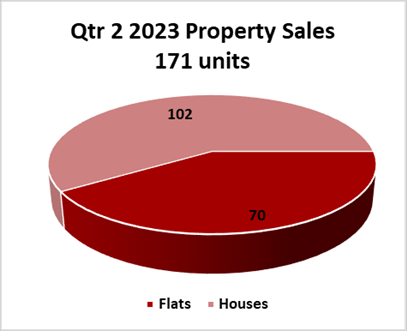

Last year, we reported that 103 houses went under offer in Q2, and this figure has only fallen by 1 unit a year later, whilst boasting a robust average value of £883/sqft (a cooling of just 1% year-on-year) as demand continues to exceed supply in W4. Of the 102 houses that sold, only 17% had to be reduced in price to achieve a sale.

The decrease in flats sales, however, sits at an alarming 36% year-on-year as we begin to see the full impact of higher mortgage rates on the buying appetite of both young professionals and landlords. Over a third of the 70 flats sold in these three months needed the help of a price adjustment, and the average value of the total sits at a much more competitive £778/sqft.

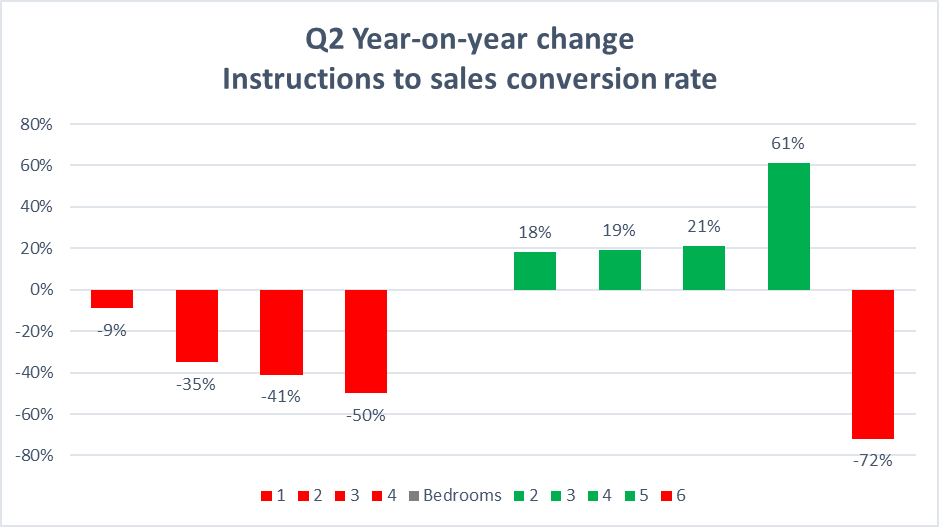

So, is it a buyers’ market or a sellers’ market?

At Andrew Nunn & Associates, we will continue preaching that it is never a bad time to sell a family home. In fact, the data shows that you are 18% more likely to sell one this year than last year, and for a similar (if not for the same) price. As for flats, with the increase in pressure to ditch sizeable mortgages, 31% less selling this Q2 than last and, consequently, competitive pricing being key for a successful sale, the evidence points towards a re-emergence of the ‘all-cash’ investor.

***********************************

Mortgage Review Q2 2023

By James Muncaster — Director, Chagnon Financial

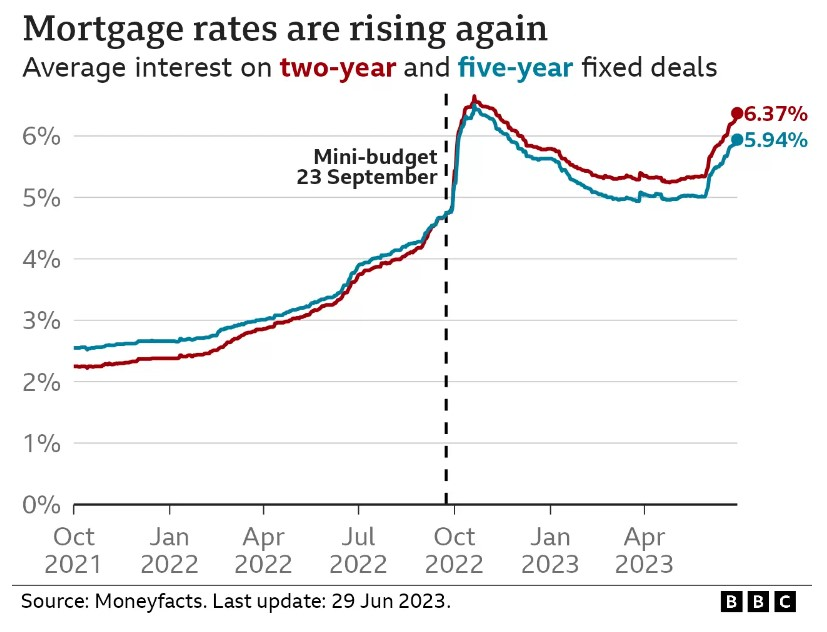

Quarter 2 was a mixed bag for the mortgage market. The start of the quarter saw reducing interest rates, following the Mini Budget impact and the Bank of England forecasting an increase in UK growth. Fast forward to the end of the quarter and the threat of a peak Base Rate of 6.25% threatens to push the UK into recession!

Average fixed rate mortgages across both 2yr and 5yr ranges have peaked to their highest for 7 months, with persistent inflationary pressure causing banks to forecast a higher Base Rate. This will impact clients coming off fixed rate mortgages in the short term but as inflation slowly comes under control, the likelihood of rate reductions will come through.

As we reach the end of the quarter, the Government has met with the leading retail banks to work out how to support those mortgage holders most affected. For those, less affected but still looking

at a remortgage, or those buyers still looking at purchasing, a lot of care needs to be taken around mortgage budget. There are three main routes for this; increase deposit/equity level, increase term or interest only. All three have merit and will help in some way to alleviate some shorter-term impact but this approach should always be with a longer term strategy in mind.

***********************************

By Katherine McDowall — Lettings, Andrew Nunn & Associates

Unsurprisingly, given the continued supply and demand imbalance, the market remained robust in Q2, albeit with a more considered audience, and rents continued to rise.

Instructions

The number of new W4 instructions in Q2 (489) was almost identical to that of Q1 (490). Naturally, flats dominated the instructions this spring, with just 18% (88) of new properties coming onto the market providing an option for those in search of a house.

Of the 401 flat instructions, 1-bedroom flats were ‘most improved’ when comparing to last quarter – an increase of 13.2%. As for the 88 houses that came onto the market, 4 and 6-bedroom houses saw an increase in market share of 57.1% and 66.6% respectively. 3-bedroom house instructions, however, dropped some 36.6%. Of course, the market is seasonal and we would expect these family homes to come up in the Spring/Summer months, which is reflected in these figures.We have noticed some ‘accidental landlords’ entering the market since the start of the year, although this ‘top up’ of supply remains some way off the levels needed to fulfil the demand. Hence, tenants are likely to continue facing frustration when searching and budgeting for their move.

Demand

Last year, we reported that properties were letting within the first few days of coming onto market; this urgency among tenants has cooled slightly and in Q2 of this year, we recorded an average period of 13.3 days for flats and 10.9 days for houses from the day of launch to securing a tenant. That said, the volume of enquiries is only marginally down – 1.9% and 2.7% respectively – when comparing to the same period in 2022, and our number of lets in Q2 is coincidentally unchanged year-on-year. With the increase in stock in the flat market, tenants are approaching viewings with less pressure to offer, whereas it is clear that the low volumes of houses coming available has led to faster lets as the demand for these remains unaltered.

Values

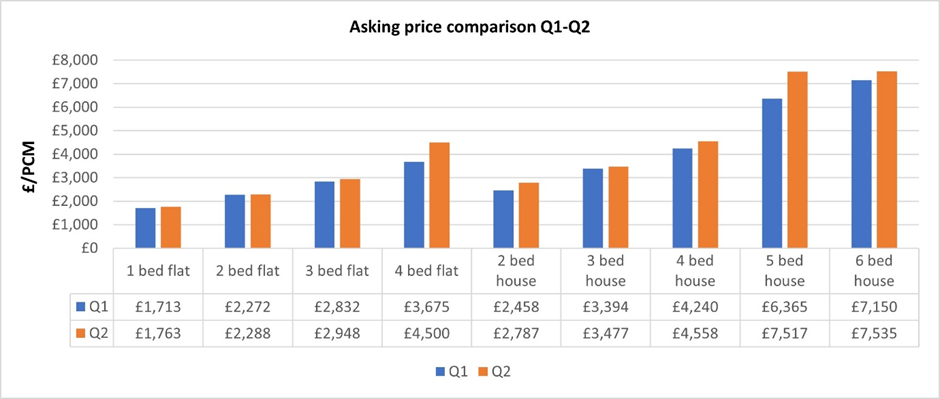

Rents are continuing to rise and our records are showing they have risen on average by a further 5-10% on last year, bringing the increase on the pre-pandemic averages to 25-30% (or more!). The average one-bedroom flat now achieves £1763pcm in comparison to £1408pcm in 2019, and the larger family homes can now command £7500pcm, an increase of £1750pcm in the last four years.

With rents having increased more than the average household’s income has risen, tenants are having to either sacrifice the size, style or location of their next property. Furthermore, tenants are now 69% more likely to renew their existing tenancy, in most cases for increased rents.In such a strong market, it can seem appropriate to ‘push the parameters’ on price; but, as the data shows, with 22% of flats and 25% of houses having needed a price reduction to secure a let in Q2, this can slow the marketing process and potentially lead to a void period. This is a stark contrast to the last year where reductions were few and far between. At Andrew Nunn & Associates, we pride ourselves on our knowledge of the market and value our properties accordingly, reflected in the fact that only 8% of our lets agreed in Q2 required a price reduction to achieve an agreement in Q2.

***********************************