Published: 11/04/2024 By Mateo Asminian & Katherine McDowall

Sales Review Q1 2024By Mateo Asminian — Sales, Andrew Nunn & Associates

The year got off to a promising start in the Chiswick property market following news in December that the Bank of England would not increase base rate from 5.25%. January saw many lenders cut their mortgage rates, stimulating buyers and giving confidence to ven dors. However, these cuts were short lived. Experts’ predictions of a base rate decrease around May were pushed back to August following news that inflation had crept back up to 4% and, with school half terms drawing closer, the market appeared to cool in February – not atypical. But sentiment changed once again heading into the last month of the quarter as we saw inflation cool and mortgage rates settle once again.

Flats show encouragement Fewer reductions needed to sell Instructions House values up 4% y-o-y Seasonality returns for family houses

Instructions

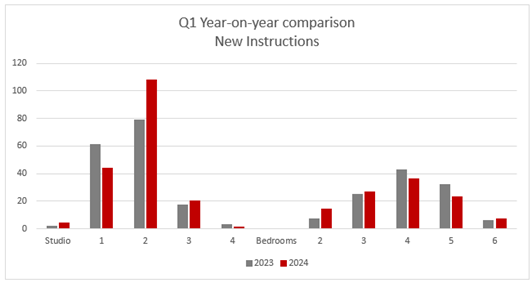

Generally, the volume of new properties that came onto the market in Q1 was greater this year (284) than in 2023 (275) – which, following four quarters of the opposite, is a very en couraging change in sentiment and proves what many have sensed already: the mood is improving.

Larger family home instructions remained short on their year-on-year comparisons, although this trend is as expected as we continue to see a return to the market’s seasonality following a few years of all-year-around activity. Those selling 4- or 5-bedroom houses nor mally plan around the main school holidays, with summer being an opportune period in the year to move, and hence a large chunk of these houses are introduced to the market in the spring (Q2).

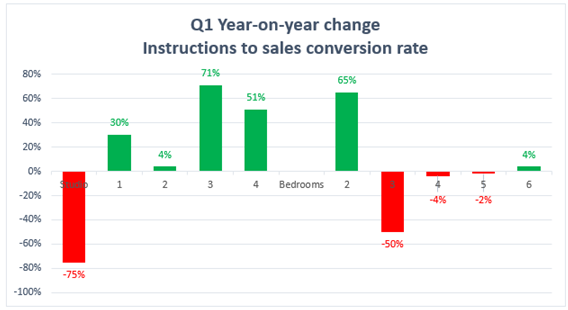

As shown in the graph, 2-bedroom flat instructions improved some 37% year-on-year, while 1-bedroom flats fell by around 28%. The reasons for these drastic changes remain unclear and we should have a clearer understanding as the year progresses. However, when you ‘zoom out’, flat instructions were up almost 10% year on year. With 3 out of 4 rental homes in W4 being flats, this growth is largely attributed to landlords beginning to take advantage of the CGT incentives introduced to them by the Chancellor in March’s budget.

Sales Agreed

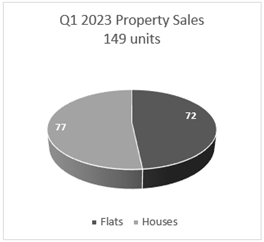

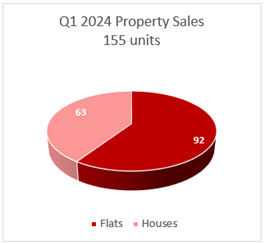

Like instructions, sales in W4 saw growth on their year-on-year figures, beating Q1 2023’s 149 units by 6.

In the two years leading up to 2024, we recorded a consistent downtrend for flat values, with the average value for flats of the previous 8 quarters (or 2 years) sitting at £772/sqft. It appears, however, that this correction is reaching its conclusion; not only did more flats sell in the first three months of this year when comparing with 2023, but the average value of flats that sold sat at exactly £772/sqft! What’s more, the amount of flats needing a price reduction before going under offer was down from 38% in Q1 2023 to just 22% this year.

Could we finally be seeing the ‘local bottom’? The demand for flats that AN&A has marketed so far this year has been very reassuring and, when priced correctly, they are attracting nu merous enquiries and multiple offers. Rent increases in recent years have undoubtedly played their role in this trend, given a considerable chunk of the flat target audience com prises first-time buyers coming out of rented accommodation. Of course, mortgage rates are now settling making repayments far more attractive, and some lenders have been in creasingly creative with their loan-to-value options, making saving for a deposit a lot less daunting for those looking to take their first step onto the property ladder. We have especial ly noted excellent demand for well-presented properties that fall within the two key tiers for first-time buyer stamp-duty relief - £425,000 and £625,000.

For houses in W4, there is never too much concern, and this quarter is no different. On the one hand, less houses sold in Q1 of this year than last year; but, on the other, and as ex plained above, this can be attributed to both the drop in house instructions year-on-year, as well as the return of the market’s ‘seasonality’. Chiswick’s houses are largely occupied by families, for whom the summer holiday is an opportune time to move. These families are more likely to be be out looking and offering in the spring months, and understandably, some of Q1’s housing stock will have required patience in allowing demand to catch up before be ing snapped up, which we are likely to see in Q2. Values for houses remained strong – up just over 4% (or £36/sqft) on their Q1 2023 average of £848/sqft – and the amount needing price reductions before going under offer was also down from 35% to 22% year-on-year.

Did you say “good news”?

Yes, we did. When we talk about Chiswick’s ‘safety-blanket’ in challenging times, this is what we mean. This desirable area will always sustain a supply/demand imbalance that under pins values and/or expedites recovery from small blips.

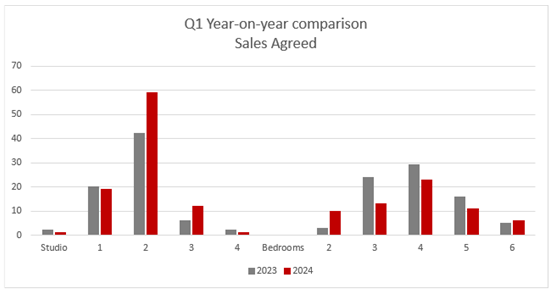

On a whole and as demonstrated on the graph, Chiswick property was more likely to sell in Q1 of 2024 than in the same quarter a year prior. On the surface, studio flats and 3-bedroom houses appeared to be much less popular in Q1 of this year than last year. Studio flats are few and far between, meaning the slightest change to the volume of instructions or sales will lead to anomalies. As for 3-bedroom houses, almost 40% of those marketed in Q1 were launched in March – if it hasn’t sold already, it will almost certainly sell in Q2.

* * * * * * * * *

Lettings Review Q1 2024

By Katherine McDowall — Lettings, Andrew Nunn & Associates

The imbalance between demand and supply continues to underpin high rent levels however there is evidence again in Q1 2024 to suggest this dynamic is cooling, that certain properties are taking a little longer to find a tenant and that in 27% of cases a price reduction has been required in order to attract the right tenant. In Q1 both the number of new instructions and the number of new applicants fell proportionally. Q1 is seasonally a quieter quarter for houses and that may explain the increase in time taken to find a suitable tenant for those properties.

Instructions

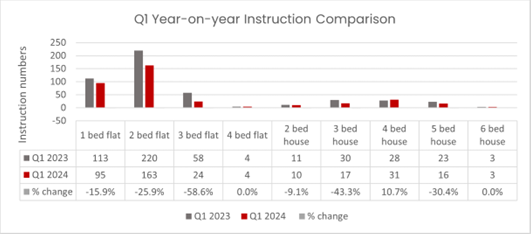

The total number of flat instructions in Q1 2024 is 27.6% down on Q1 2023 comprising a drop of 15.9% for 1-bedroom flats (113 – 95) and a drop of 25.9% for 2-bedroom flats (220 – 163). This is possibly reflective of more landlords selling off their investments as mortgage rates continue to rise and many portfolio landlords face punitive loan reviews by their historically consider ate lenders. We have also seen a significant rise in the number of tenants moving out of 1 and 2 bedroom rental properties and into the buying (ownership) market as the cost of servicing a mortgage compares favourably with current rent levels.

House instructions also fell overall by 18.9% when comparing Q1 2024 to Q1 2023 with 3 and 5 bedroom units making up the lion’s share of this drop.

This drop reflects some accidental landlords continuing to sell their assets and other land lords managing their tenancies to ensure they come to market in the busier spring/summer months. We anticipate an increase in stock level in Q2 and Q3 when the high numbers of 2022 “2 year lets” come to an end.

Demand

Applicant registrations are 19% down Q1 2024 versus Q1 2023 which continues the steady de cline in applicant enquiries over the past 18 months. Viewing numbers are up 61% for the same period which suggests applicants are considering more properties and searching for “value for money” before selecting their preferred property. Statistically it now takes on aver age 29 days to let a house compared to a year ago when it was 16 days to let a flat compared to 12 days a year ago.

Values

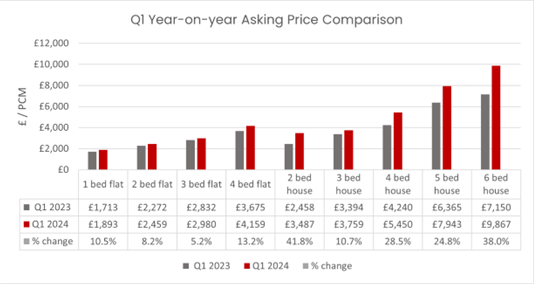

Average rents for flats have increased by 9.5% year-on-year with 1-bedroom flats now commanding £1893pcm, being a 10.5% increase, and 2-bedroom flats a hefty £2459pcm which is 8.2% up on a year ago. This increase, supported by fewer applicants, has been driven by the 27.6% reduction in the number of flats coming to market. Rental values for houses appear to have improved quite dramatically year-on-year with an average increase of 29.2% across all sizes. 2-bedroom houses lead the way with a huge 41.8% increase, however supply of houses fell by 18.9% over the same period and so we suggest a part of the significant in creases in rental levels comes down to the relatively small sample size potentially exaggerating the number for this period.

With a combination of falling instructions in Q1 in contrast to the rapidly rising values creates the potential for values to overshoot, and with an expected uplift in instructions in Q2 and Q3 but similar levels of demand, we would suggest landlords apply a little caution when setting asking prices over the next few months.

It is worth noting that in Q1 2024, 34% of houses required a price reduction in order to secure a tenant, whilst 20.6% of flats were reduced during their marketing period. This compares to 25% of houses needing a reduction in Q4 2023 and 23% of flats. The data compiled for Q1 2024 suggests properties may have over shot their market rent level and so more price adjust ments will be required, albeit at rents which are still far higher than the pre-pandemic levels.

Yields

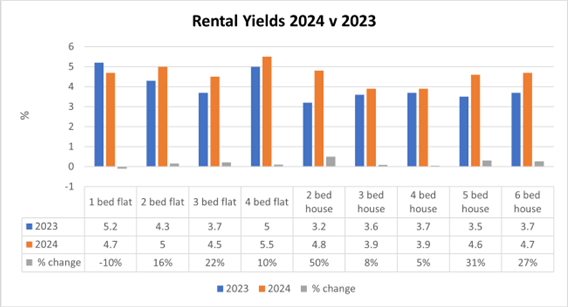

With the exception of 1-bedroom flats, yields have seen strong increases year-on-year with rising rental values and flatlining capital values being the basis for this dynamic. The rising cost of buy to let mortgage money suggests that rental yields need to settle around 5% - 6% to make property investment attractive and even then the investor market will need to feel that they will be getting steady capital growth alongside the rental return.

* * * * * * * * *

Mortgage Market Review Q1 2024

By James Muncaster — Sales, Chagnon Financial

As we navigate through the first quarter of 2024, we’ve observed a lot of changes in the UK mortgage market that are worth highlighting.

The Bank of England’s decision to hold the Bank Rate steady at 5.25% reflects a cautious opti mism in the economic landscape. With inflation data falling, the year started fast with mar kets predicting 5-6 rates cuts in 2024. This led to January activity being good and lots of pos itivity in the market. The February market slowed as rate started to climb back up. This was off the back of worse than expected financial data and the banks correcting their pricing. In March, we started to see falls again, as the data improved again! It looks volatile but the rate changes were marginal rather than the large swings we saw in 2023. With the markets now predicting 2 Base Rate cuts in 2024, rate setting has been much more stable as we close out the quarter.

What this does highlight, is the value of using a mortgage broker who is “on the ball”. Trying to watch rates on your own while dealing with the rest of your work and life would be almost impossible, with banks being very reactive to markets and changing rates on a daily basis. As the year progresses, expect to see further cuts in fixed rates but also the start of the return in tracker and variable rates, as Base Rate cuts start.

There has also been some notable moves from banks in terms of policy. We have seen the launch of the 99% mortgage by Yorkshire Building Society for First Time Buyers. With that end of the market harder, with higher rates and harder ability to borrow, it is good to see some innovation and an attempt to help First Time Buyers.

We have also seen some banks introduce 1 Year Fixed Rate mortgages. Again, with the mar ket still in a state of flux, postponing your longer term rate decision can be a useful thing. Also, it does stop clients risking a variable or tracker rate if they feel that is nor for them Looking forward, there is still plenty of optimism in the mortgage market. Banks will see some improvement in affordability after the tax changes in the Budget. This will benefit some but not all.

As we get closer to the General Election, we may see a drop off in activity. It will be interesting to see if banks are “on target” and those that are not may see an opportunity as the year closes. I am expecting to see a busy summer, however, with most decisions made before the GE.

* * * * * * * * *