Published: 07/04/2025 By Mateo Asminian & Katherine McDowall

Sales Review Q1 2025By Mateo Asminian — Sales, Andrew Nunn & Associates

After a year that saw the first (and eagerly anticipated) base rate cut in almost four years, 2025 began with notable improvement in sentiment and activity in the property market in Chiswick, with hopes of some more positive rate announcements – and, consequently, bet ter mortgage deals – being supported by the forecasts in the media. At the start of the quarter, mortgage rates were ranging between 4-5%, inflation was only half a percent above BoE’s 2% target and home buyers were snapping up January stock with hopes of completing before the SDLT relief deadline of the 31st March. February, a typically quiet month in the property market in Chiswick, saw the first of the year’s drops in base rate to 4.5%, followed by a wave of lenders trimming their mortgage deals and, at last, we saw mortgage rates dip below the 4% mark! By the time the cherry blossoms began to bloom, it was clear that the property market in Chiswick was heading in the right direction.

Instructions up 21%

Values strengthen by 3.5%

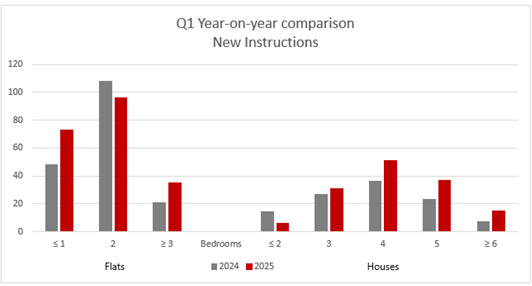

Instructions

Volume of sales improves

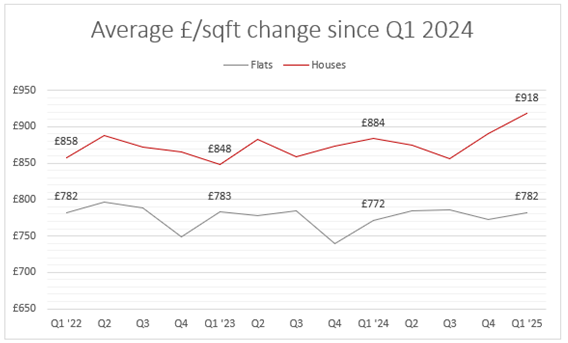

Flat values continue to strengthen

Instructions

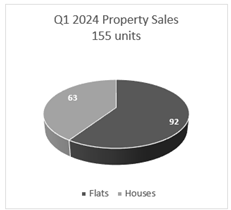

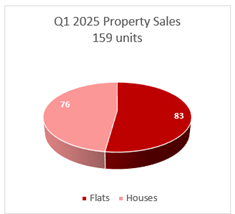

In Q1 of 2024, we reported a slight improvement of 3.3% year on year in the volume of new properties being introduced to the market in W4 – a welcome reversal to four quarters of stock levels going the other way in 2023. The first three months of 2025, however, have completely outperformed Q1 of last year, with the pool of new instructions increasing by a whop ping 60 units (or 21%) to 344.

The decline in 2-bedroom flat instructions does not come as a great surprise with an estimated 3 out of 4 rental properties in Chiswick being flats and as we see the ‘landlord exodus’ fizzle out.

By default, the market for smaller houses (of 2 bedrooms or less) is more niche and, therefore, even the subtlest increases or decreases in the number of units introduced to the market is always likely to cause anomalies.

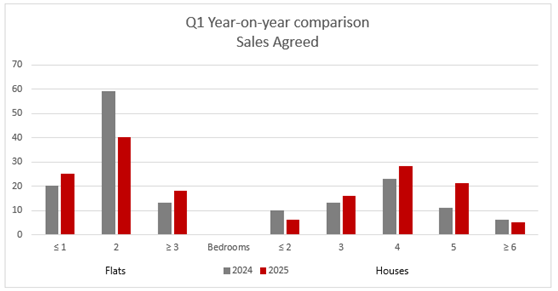

Sales Agreed

The sales data for the quarter appeared to follow that of new instructions closely, with the market producing more sales within the first three months of 2025 than the same three months in 2024

House sales remained robust, despite the busier three months of the year for this section of the market still being ahead of us. Only small houses (up to 2 bedrooms) and the largest houses (6+ bedrooms) saw declines on their year-on-year figures.

That said, the devil is in the detail, and for these 1 and 2-bedroom houses, the number of sales (6) was largely driven by the total number of units made available in the quarter (6), which paints a more encouraging picture. 6+ bedroom houses were down by just 1 sale year on year and it is no secret that the market for these truly comes to life in the spring - we would expect the unsold houses of this size to be snapped up in the coming months.

The following data is for those of our readers who have are considering selling but are unsure about the market. The average flat value per square foot has improved some 1.3% when comparing with that of Q1 in 2024, as lenders’ loan-to-value flexibility and attractive rates continue to make buying more attractive than renting, improving first-time buyer demand. The headline, however, will undoubtedly be dominated by the increase in values for houses, with their average value per square foot in Q1 of 2025 sitting at £918, an impressive increase of £34/sqft or just under 4% year on year! This marks the second year in a row where house values have increased by over 3% in Q1; although, this time, only 18% of the houses that sold in the quarter needed a price reduction to attract a buyer – down from 22% Q1 of 2024.

The future is bright...

The first quarter has given us plenty of reason to be optimistic about the market in Chiswick and, here at AN&A, we are gearing up for another busy spring. Values, as demonstrated in the graph below, are on the right trajectory; flats prices are experiencing far less volatility after a tricky few years of rampant inflation and increasing interest rates unsettling buyer and vendor sentiment and house prices are demonstrating that there is no ‘ceiling’. If you are considering selling your home this spring, please get in touch with us to arrange a valuation of your property – we are sure that we can add value to your sale.

* * * * * * * * *

Lettings Review Q1 2025

By Katherine McDowall — Lettings, Andrew Nunn & Associates

Q1, normally the most subdued quarter in the year, saw trends of late continue to intensify with growing demand, limited supply and a readjustment on rental values. But could there be an opportunity for new or existing landlords to capitalise on this? Our independently collect ed data detailed in this newsletter shows some downward trends year-on-year, however when comparing the data from two and three years ago we have found that rents for both flats and houses are much improved suggesting that pricing in 2024 and Q1 2025 simply overshot what the market could sustain. It remains positive for investors and landlords that rents are still high, but that we need to be more mindful of pricing competitively for the current market.

Instructions

The first quarter of 2025 has seen a reduction in the number of rental properties coming onto the market in Chiswick, following the trend from last year. The total number of instructions in Q1 2025 is down 22.8% year-on-year, as we continue to see the effect of increased mortgage costs, past taxation changes, and upcoming regulatory reforms (e.g. potential changes un der the Rentors Rights Bill).

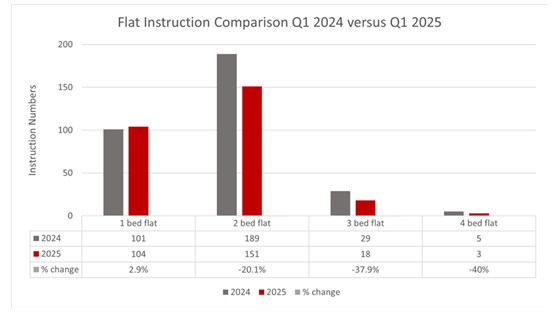

Flat instructions have dropped by 14.8% overall, largely driven by a sharp fall in the number of two-bedroom (-20.1%) and three-bedroom (-37.9%) properties coming to market. However, one-bedroom flats saw a slight increase of 2.9%. Our data shows that rents for these units are generating the strongest yields therefore a more attractive proposition to hold on to.

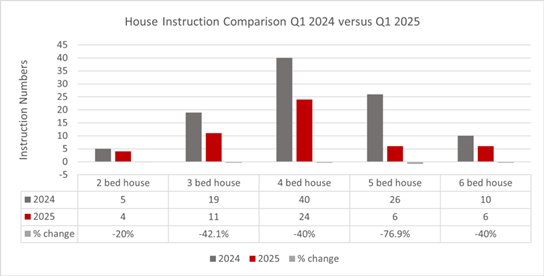

House instructions have experienced a steep decline, down 49% compared to Q1 2024. The most significant reductions were seen in the five-bedroom (-76.9%), three-bedroom (-42.1%), and four-bedroom (-40%) segments. Although the first quarter of the year is not seasonally the best time to market houses the year-on-year analysis does still show the annual decline in supply. We have found that with less houses coming available, tenants are choosing to renew their existing tenancies, which has contributed to the lower stock levels. However, this increase in renewals provides stability for landlords, ensuring continuous rental income with minimal void periods. Moving forward to the Spring/Summer months there is an opportunity to introduce new properties to the market to match growing demand.

Demand

Applicant registrations surged by 40% in Q1 2025 compared to the same period last year, in dictating a growing number of tenants exploring their options. However, despite this sharp rise in enquiries, viewing numbers have increased by a more modest 9.2% year-on-year, trans lasting to an -8.2% conversion rate.

From the enquiries we have received, it's clear that many applicants are casting a wide net - registering interest in multiple properties across different areas without thoroughly reviewing details or locations beforehand. As a result, fewer of these initial enquiries are turning into actual viewings.

That said, there are positive signs: offers for us are up 12% year-on-year, and lets agreed have risen by 14%, indicating that while tenants are taking longer to decide, committed movers are still entering the market.

We’re also seeing a shift in tenant behaviour. Rather than rushing to secure a property ahead of the competition, applicants are taking more time to compare locations and explore their options. This change is reflected in the average time to let, which now stands at 22 days in Q1 2025. Additionally, nearly 25% of listings required a price reduction before securing a tenant, underscoring the importance of strategic pricing in the current market.

Values

In the first quarter of 2025, we’ve observed further shifts in the rental market in Chiswick, with notable downward changes in asking rents for both flats and houses when compared to the same period in 2024. Wider economic factors, such as inflation, interest rate hikes, and concerns about the cost of living, can impact tenants’ ability to pay higher rents and this has led to a shift in demand towards more affordable rental options or a reluctance to move. Whilst landlords may have higher mortgage costs to cover, it is tenants who are also influencing rental prices.

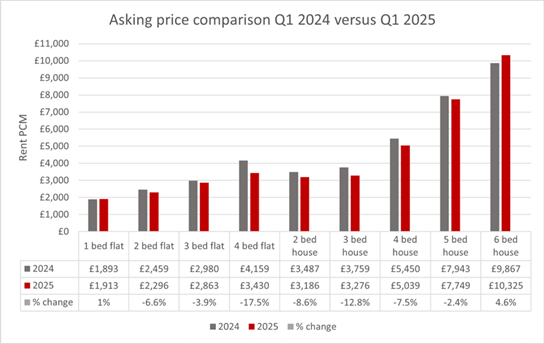

For flats, the average asking rents have mostly decreased. One-bedroom flats did see a slight increase of 1%, rising from an average £1,893pcm in Q1 2024 to £1,913pcm in Q1 2025. However, two-bedroom flats have experienced a 6.6% drop, with rents now at an average £2,296pcm, down from £2,459pcm last year. Three-bedroom flats followed suit, seeing a de crease of 3.9%, with rents now averaging £2,863pcm, down from £2,980pcm.

Looking at houses, the trend continues with a decline in asking rents across most categories. Three-bedroom houses have decreased by 12.8%, with rents now averaging at £3,276pcm, down from £3,759pcm. Four-bedroom houses saw a decrease of 7.5%, now at £5,039pcm, compared to £5,450pcm last year. Five-bedroom houses experienced a 2.4% decrease, now renting for an average £7,749pcm, down from £7,943pcm. Six-bedroom houses were an ex ception, with rents increasing by 4.6%, from £9,867pcm in Q1 2024 to £10,325pcm in Q1 2025, although their sample size was smaller with just 6 coming to market.

Overall, the total rental values for flats and houses have dropped by 4.5% year-on-year. Flats as a whole have seen an 8.6% reduction, while house rents have decreased by 3%. This reduction in rental values comes amidst a market where supply has started to stabilise, and demand remains relatively steady but at the right price. Given the fluctuations in rental prices and price reductions being witnessed, pricing sensibly is best and to minimise the possibility of a void period. However, landlords with well-maintained and correctly priced properties are in an excellent position to secure tenants efficiently.

While rental values are adjusting from the last few years highs, demand for well-presented, correctly priced properties remains robust. With a 40% increase in applicant registrations, landlords with available properties are still in a strong position to secure tenants and we must not forgot that whilst rents might be stabilising they are still much higher than prior to the pandemic.

Despite some fluctuations, Chiswick remains a highly desirable rental market, and properties that align with current tenant expectations continue to perform well. The key takeaway for landlords is that properties offering good value in the current climate are letting efficiently, ensuring steady rental income and minimal void periods.

Renters’ Rights Bill

The Renters’ Rights Bill is currently making its way through Parliament and is expected to bring some significant changes to the private rental sector. While the finer details and imple mentation timeline are still being finalised, it’s worth having a general awareness of what’s to come. Key proposals include the end of fixed-term tenancies, making periodic tenancies the norm, and the abolition of Section 21 ‘no fault’ evictions. While this will change how we/landlords manage tenancies, the government has committed to strengthening the Section 8 process and court system to ensure landlords can still regain possession in reasonable circumstanc es—such as rent arrears, antisocial behaviour, or if they need to sell or move back into the property. Understandably, some landlords are concerned about losing flexibility, particularly around ending tenancies. However, in our experience, it's rare for notice to be served due to tenant behaviour. Most landlords only do so when they need the property back or plan to sell. Thanks to our thorough referencing process and careful applicant vetting, the tenants we place are reliable, respectful, and treat their rental homes well and so we do not expect this bill to be of too much concern. In many cases, longer tenancies can mean fewer void periods and more consistent income— something many of our landlords already benefit from. The proposed changes also offer an opportunity to create greater transparency and trust between landlords and tenants, which can lead to smoother management overall. We’ll continue to monitor developments and will provide updates as the Bill progresses. If you’d like tailored advice on how these changes might affect your property, please do not hesitate to contact us.

* * * * * * * * *