Published: 02/07/2024 By Mateo Asminian & Katherine McDowall

Sales Review Q2 2024By Mateo Asminian — Sales, Andrew Nunn & Associates

After a positive first three months of the year, largely thanks to the ‘New Year bounce’ and attractive mortgage rates, many were anticipating a busy spring in the W4 property market. The Easter school holidays, which normally bleed some momentum out of the market, came early this year, and the subsequent activity in April appeared to be the start of another competitive market for buyers. In fact, over 40% of the quarter’s sales were ultimately agreed in this month. May, however, saw new listings and, consequently, sales decelerate, with the W4 public’s attention turning to the Early May Bank Holiday, the half term and, most significantly, the announcement of the date for the general election on the 22nd May. As we entered June, 2-year mortgage rates were up 17% since the beginning of the year, the sun had made its long-awaited appearance and the hot topic was “can Southgate bring it home"

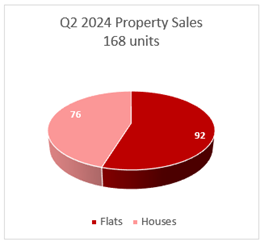

Flat values improve—first increase since 2022 Flat sales up 60% Instructions Fewer reductions needed for houses Total sales almost unchanged

Instructions

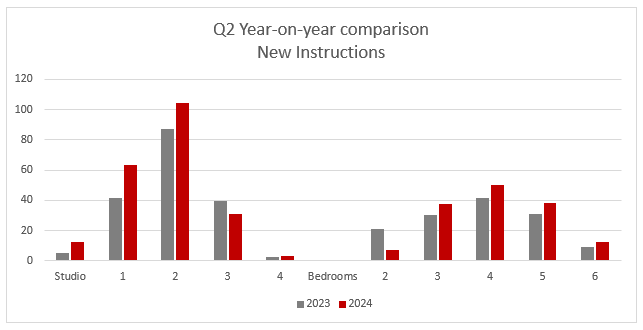

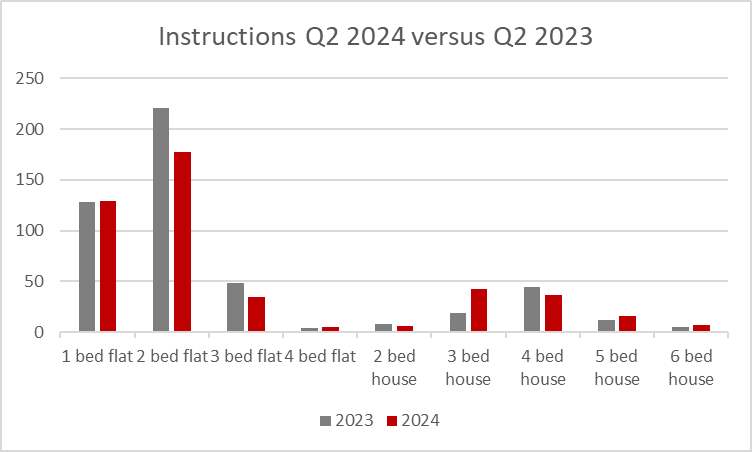

For the second quarter in a row, stock levels in W4 grew year-on-year – this time by 17%. Of the 10 categories on properties within the table below, only 2 (3-bedroom flats and 2-bedroom houses) showed drops in their figures this year.

It’s safe to say that the date of the general election came as a surprise to us all – psychics and Tory ministers aside, of course... The general sentiment was that we would see a change of government in the autumn, making the spring the most opportune season to sell for those Chiswick homeowners planning a move in 2024. This translated into an uplift in stock with an average of 31 new properties being introduced to the market per week between the beginning of the quarter and the announcement on May 22nd – some 30% more listings per week than in the succeeding 5-and-a-half weeks that made up the quarter.

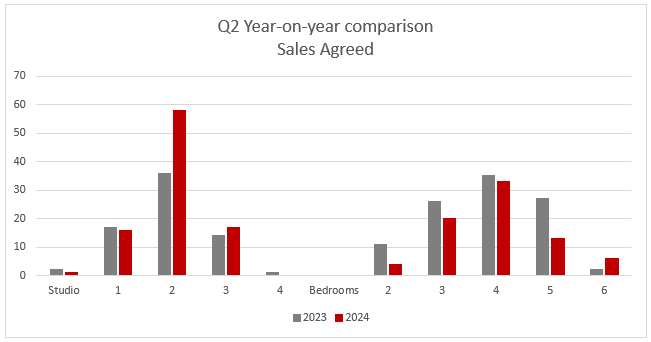

Sales Agreed

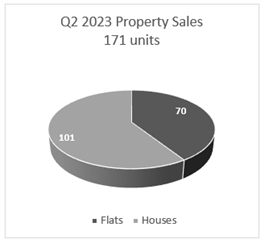

The total number of sales agreed between the beginning of April and the end of June this year was only 3 units off the 171 in the same period in 2023.

So, should I wait to sell?

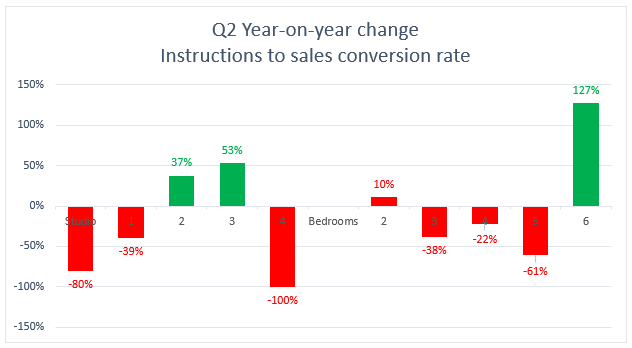

The general election has always and will always influence the property market to some degree. The below graph shows that some properties were unaffected while others felt this slowing more. However, with values remaining strong, we are not concerned. As we enter the summer, we should expect similar activity levels to those seen in the last few weeks – a typical summer – but, we are expecting a busy autumn. Now might be a good time to consider the ‘off-market’ strategy for Chiswick homeowners lining up a move in the autumn. This discreet method of selling comes with little exposure to the vendor, and we can often introduce highly motivated buyers who would be prepared to pay a premium for the exclusivity. If you would like to explore this, please don’t hesitate to get in touch.

Lettings Review Q2 2024

By Katherine McDowall — Lettings, Andrew Nunn & Associates

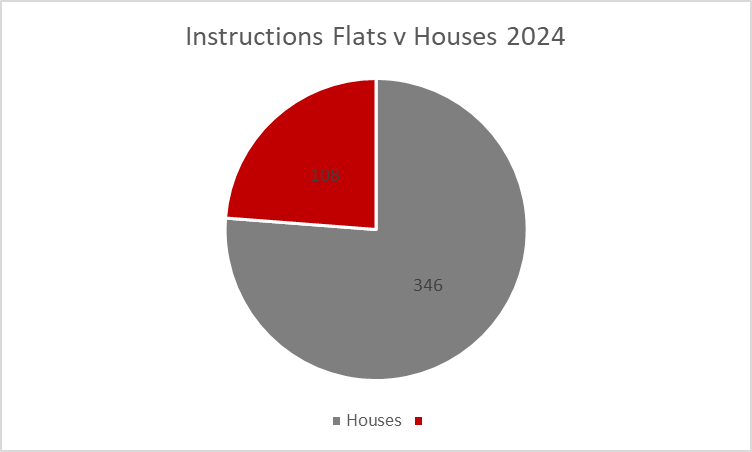

The imbalance between demand and supply continues to underpin high rent levels, with instructions down 7.2% and applicants up 17% when comparing Q2 2024 to Q2 2023. However, there is evidence in Q2 2024 to suggest this dynamic is cooling, that certain properties are taking a little longer to find a tenant and that in 18% of cases a price reduction has been required in order to attract the right tenant. In Q2 demand for houses tends to kick in and this has been evident in the property types we have agreed toward the end of the quarter. Instructions The total number of flat instructions in Q2 2024 is 13.7% down on Q2 2023 comprising a drop of 19% for two bedroom flats (221-177) and a drop of 27% for three bedroom flats (48 – 35). This is possibly reflective of more landlords selling off their investments as mortgage rates fail to drop as quickly as expected. We have also seen continual rise in the number of tenants moving out of rental sector and into the ownership market, as the cost of servicing a mortgage compares favourably with current rent levels. By contrast house instructions rose by 22% when comparing Q2 2024 to Q2 2023 with three bedroom properties up a whopping 121%. The increase in house instructions is partially due to many long term post lock down contracts coming to an end in 2024.

The number of four bedroom houses fell by 15.9%, which, again, may be a reflection that some landlords are still looking to sell their assets rather than re invest in them to bring them into line with the exacting standards required in 2024.

Demand

We have seen a reversal in trend here with applicant registrations up 17% Q1 2024 versus Q1 2023, which may reflect the increased number of people coming back into town and to their workplace offices. Furthermore, as properties take a little longer to rent, they are likely to generate more enquiries from more applicants. Viewing numbers are up 21% for the same period suggesting applicants are considering more properties and searching for ‘value for money’ before selecting their preferred property. Statistically, it now takes on average 24 days to let a house and 14 days to let a flat.

Values

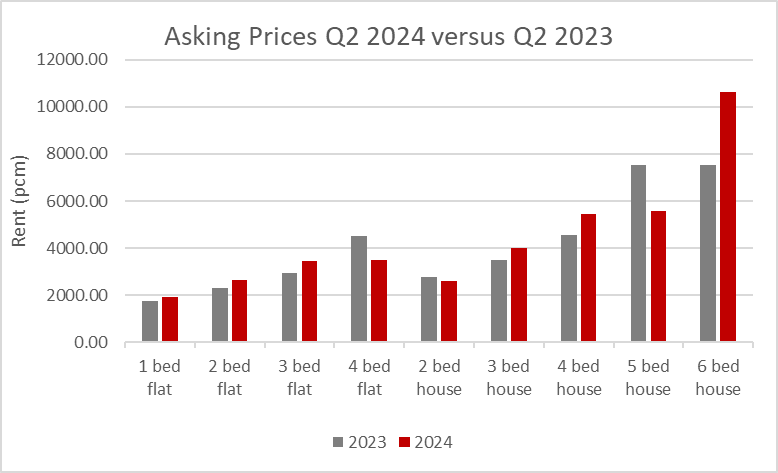

Average rents for flats have improved 8.8% when comparing Q2 2024 to Q2 2023, with one bedroom flats increasing by 9.9% to £1938pcm and two bedroom flats up by a whopping 16% to £2653pcm. This increase, supported by more applicants, has been driven by the 13.7% reduction in the number of flats coming to market. Rental values for houses appear to have improved significantly year-on-year with an average increase of 9% across all sizes. Three and four-bedroom houses lead the way with 15% and 19% increases respectively, giving average monthly rents of £4014 and £5433. Overall the supply of houses increased by some 22.7% which reflects the number of two year post lockdown tenancies coming to an end. With a combination of falling instructions in Q2 in contrast to rising values we envisage a steady summer/autumn market as applicants pick out ‘best-in-class’ properties.

It is worth noting that in Q2 2024, 13.8% of houses required a price reduction in order to secure a tenant whilst 19.5% of flats were reduced during their marketing period and whilst this compares favourably to the previous quarter it emphasis that the market is transitioning. The data now compiled for Q1 and Q2 2024 suggests many properties may have over shot their market rent level and so more price adjustments will be required, albeit at rents which are still far higher than the pre-pandemic levels.

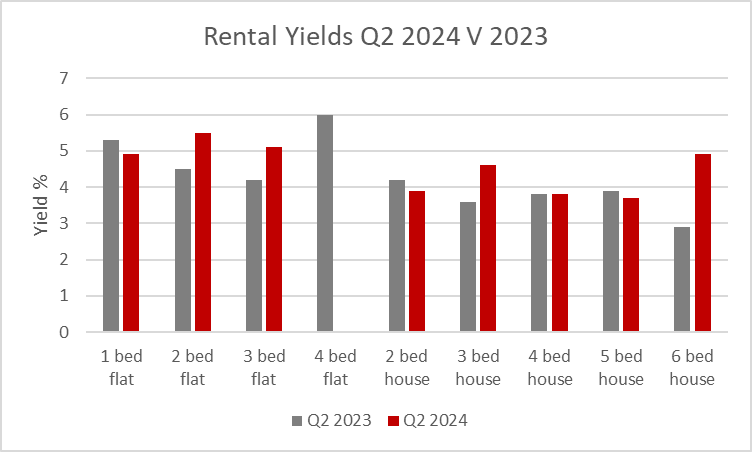

Yields

Average yields are marginally improved year on year with flats increasing to 5.1% and houses to 4.2% the uplift being fuelled by low or static capital growth and increasing rental values. With the cost of buy to let finance not falling as expected then rental yields will need to settle around 5% - 5.5% to make property investment attractive and even then the investor market will need to feel that they will be getting steady capital growth alongside the rental return.