Published: 14/07/2025

Sales Review Q2 2025By Mateo Asminian — Sales, Andrew Nunn & Associates

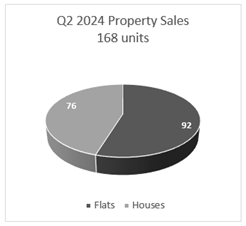

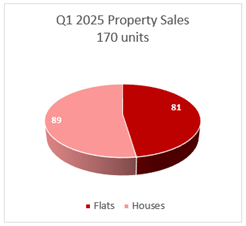

The property market in W4 entered the quarter with a notable drop off in activity, largely attributed to buyer and vendor caution following the SDLT changes that took effect on April 1st. As a result, April only accounted for less than 30% of the quarter’s total sales. However, the BoE’s decision to drop base rate to 4.25% and the consequent improvement of mortgage rates in May saw the market gain momentum and led to almost 10% more sales agreed month-on-month. On paper and in hindsight, considering both the political and economic landscape in the UK and also the general global geopolitical outlook (both of which typically influence the property market), June should have been a quiet month. Yet, once again, W4 demonstrated a now-familiar resilience in the property market, with the last month in the quarter being responsible for almost 40% of the total number agreed in the three months.

* Stock levels increase * Sales almost unchanged

Instructions * House values improve again * Flat values see slight dip

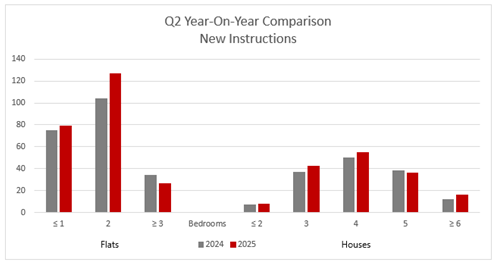

Here at Andrew Nunn & Associates, we harvest data at the end of each quarter to review how each period in the year has fared. The data we collected over Q2, displayed in the table below, showed an encouraging improvement of 9% on the total stock level, year on year.

The most notable increase of all categories of property was the 2-bedroom flat, with 22% more made available to buy between April and June of this year than the same period last year. An estimated 70% of all rental properties in W4 are flats, with more than half of those falling into the 2-bedroom variety and, therefore, it is no surprise to see an uplift in the amount that have come onto the market when also considering the imminence of the new Renters’ Rights bill and the ‘landlord tax’ changes of recent years and the consequent dampening in demand for investment property.

Only larger flats of 3-or-more-bedrooms (an already ‘niche’ market) and 5-bedroom houses (down just 2 units in total) failed to improve on their stock levels of the same period last year - nothing of significance to report here.

Sales Agreed

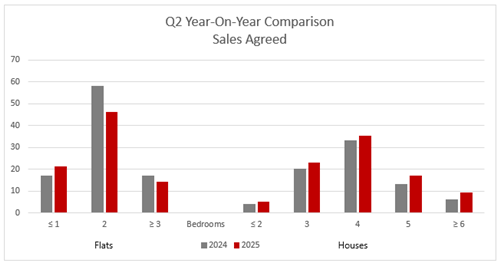

Overall, the volume of sales in the quarter saw a marginal increase of around 1% year on year – but this figure fails to tell the whole story.

Flats generally saw weakened demand in Q2 of this year as the SDLT relief (which benefited the ‘lower end’ of the market most) came to an end, taking with it 12% of flat buyers in total – largely, but not exclusively, owing to the 21% fall in 2-bedroom flat sales. However, the majority of flat buyers remained in the market seeing opportunity to be more selective, evidenced by a drop of £16/sqft (or 2%) in the values of flats sold in this period, with an increase of 5%p in price reductions needed to sell year on year.

Demand for houses in W4, largely from families, continues to outperform that of flats, thanks to the area’s excellent transport links, amenities and, crucially, schooling options, with the total volume of house sales up 17% and values up £33/sqft (4%) on Q2 2024’s figures, despite 26% needing a reduction to sell – an increase of 6%p year on year.

So is it a good time to sell?

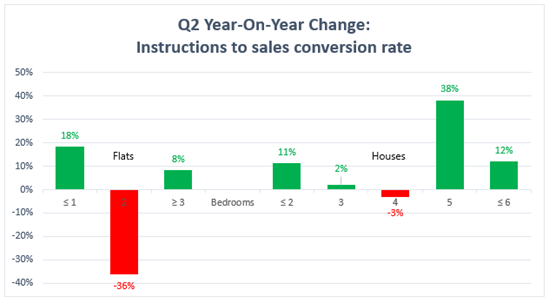

It’s never a ‘bad’ time to sell in W4; after all, it only takes one buyer to sell a property, and there are plenty of those around. In fact, the table below, which tracks the change in dynamic between supply and demand (or instructions to sales), shows that almost every category of property was more likely to sell in Q2 of this year than the same quarter in 2024.

The outlook for 2-bedroom flats appears gloomy on the surface; though, as explained earlier in this article, many of these properties have historically been held and are now being sold by landlords. We therefore anticipate supply and demand for these properties to recalibrate over the next 12-18 months as we move towards the conclusion of the ‘landlord exodus’ in the market.

Generally, the trajectory of interest rates remains promising, which should provide the public with comfort and reassurance surrounding their plans of moving and boost demand. If you are considering selling and would like to discuss your property and the market, please don’t hesitate to get in touch with us – we’re sure we can add value to your sale.

********************

Lettings Review Q2 2025

By Katherine McDowall — Lettings, Andrew Nunn & Associates

The last three months appear to have brought about some positive news - our independently collected data shows that instruction numbers are improving to meet the high levels of demand and rents are holding strong despite increased competition. Whilst rents are in creasing at a slower rate than previously reported and indeed are levelling out a little, they still remain high compared with pre-pandemic levels.

Instructions

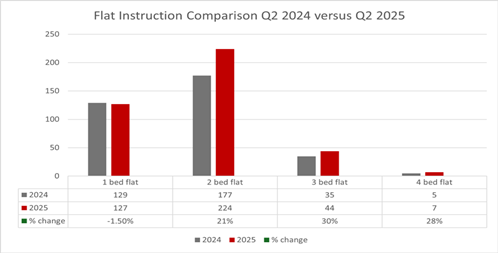

Q2 of 2025 has seen a much more positive shift in rental supply compared with both the same period last year and the last quarter. Overall, the number of properties coming to market in Chiswick has increased, with total instructions up across both flats and houses year-on-year. Flat instructions rose by 13.9% year-on-year.

The growth was driven by two, three and four bedroom flats with 21%, 30% and 28% respectively. One-bedroom flats however saw a very minor drop of 1.5%, though the unit difference is minimal and they still continue to take up most of the majority share.

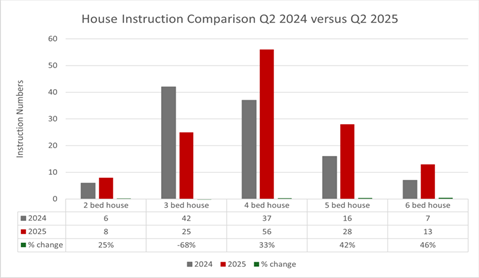

Unsurprisingly, given the usual seasonal trends of Spring/Summer, house instructions also rose, up 16.9% compared with Q2 2024. The most notable increases came from the larger end of the market: five-bedroom houses increased by 42%, and six-bedroom houses by 46%. Four-bedroom houses saw a 33% rise, while two-bedroom houses rose by 25%. The only segment to decline was three-bedroom houses, which dropped sharply by 68%. However, with not so many affordable mid size houses to move to, we have found a number of tenants renewing thus shortening the supply of new three bedroom properties coming to market.

The overall uplift in both flat and house supply points to renewed confidence among land lords, likely encouraged by a better summer market, a more stable interest rate environment and continued demand for quality rental homes. As we continue to move through the busy summer lettings period, this improved supply is helping to meet tenant demand - though accurate pricing remains essential.

Demand

Applicant registrations continue to increase with a huge 50% rise year-on-year, as to be expected with more properties coming available. Viewing numbers have also gone up by 35% which naturally has led to an increase in both our offer and let numbers, with offers up by 16% and new lets by 14%.

Overall there’s positive movement, but we do appear to have re-entered the market we saw post pandemic where applicants are presenting offers on multiple properties in the hope of securing the best deal, which can affect the offer to let ratio, and cause disappointment for landlords - so acting quickly on getting a landlords decision on an offer is paramount.

We previously reported that tenants were casting a wider net with their searches and taking longer to decide whether to proceed with offers. Now, we're increasingly seeing offers being made without genuine intent to progress, which highlights the more challenging nature of the current market. That said, the average time to let has improved slightly - now sitting at 21 days compared to 25 days last quarter. However, 25% of all instructions still require a price reduction, reinforcing the need for sensible and realistic pricing from the outset.

Values

In Q2 of 2025, the Chiswick rental market has shown a more nuanced picture when it comes to asking rents, with a clear difference between houses and flats.

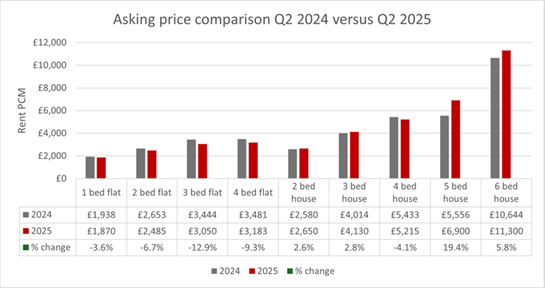

Flats have seen a broad-based decline in asking rents, down 8.7% overall compared with the same period last year. One-bedroom flats decreased by 3.6%, with average asking rents falling from £1,938pcm in Q2 2024 to £1,870pcm in Q2 2025. Two-bedroom flats dropped by 6.7% to £2,485pcm, while three-bedroom flats saw the largest fall, down 12.9% to an average of £3,050pcm. Four-bedroom flats followed suit, decreasing by 9.3% to £3,183pcm. With a 13.9% year-on-year rise in flat instructions it has given tenants more choice, reducing upward pressure on rents.

In contrast, houses have performed more strongly, with overall average asking rents increasing by 6.5% year-on-year. Two-bedroom houses rose by 2.6% to £2,650pcm, while three bedroom houses increased by 2.8% to £4,130pcm. The most significant uplift was seen in five bedroom houses, where average asking rents jumped 19.4% to £6,900pcm – most likely influ enced by a higher proportion of premium properties entering the market during the prime summer market. Six-bedroom houses also rose by 5.8% to £11,300pcm. Four-bedroom houses were the only category to see a slight drop, down 4.1% to £5,215pcm.

This variance between flats and houses may reflect broader lifestyle and affordability trends, with many tenants re-evaluating their housing needs and budgets. While landlords of flats may need to adjust expectations slightly, those with well-presented houses - particularly larger family homes - continue to benefit from strong demand and solid rental returns.

Despite these fluctuations, the overall outlook remains stable. The increase in supply is helping to balance the market, and properties that are correctly priced and well maintained are still letting efficiently. We are advising landlords to be a little flexible on pricing and to focus on presentation to secure quality tenants with minimal voids. While asking rents for flats have dipped, they remain significantly above pre-pandemic levels, and demand across the board remains resilient.

Renters’ Rights Bill

The Renters’ Rights Bill is now progressing through the House of Lords, with Royal Assent expected in Autumn and most changes coming into effect in late 2025 or early 2026.

* * * * * * * * *