Published: 09/10/2024 By Mateo Asminian & Katherine McDowall

Sales Review Q3 2024By Mateo Asminian — Sales, Andrew Nunn & Associates

The third quarter of 2024 saw buyers and sellers return to the Chiswick property market with some renewed focus. After a cautious period between Rishi Sunak’s announcement of the general election in May and the election itself in early July, activity picked up, buoyed by news that inflation had returned to the Bank of England’s 2% target. As expected, the school holidays and warm weather caused a seasonal dip in activity during August, despite the first drop in the base rate since March 2020. Inflation picked up slightly in August but held steady in September, and while the Bank of England left the base rate unchanged, mortgage rates were on average 14% more favourable at the end of the quarter than they were on July 1st , serving as a catalyst for a brisk end to the quarter.

Flat values improve again Probability of sale increases Instructions Less reductions needed to sell Volume of sales unchanged

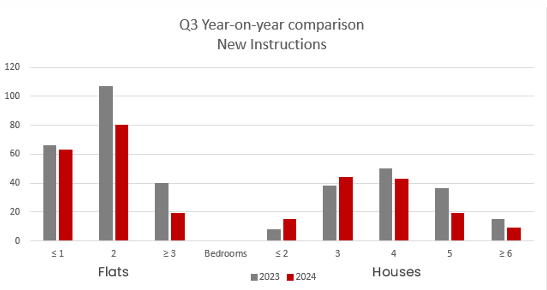

After two quarters of year-on-year improvements to stock levels in W4, Q3 saw new instructions plummet by 19% compared to the figures of Q3 in 2023. Flats saw the bigger drop in new listings with 24% less being introduced to market in July,

Flats saw the bigger drop in new listings with 24% less being introduced to market in July, August, September of this year than the same three months last year. However, this trend is as anticipated as the frequency of working from home continues to diminish and the appeal of swapping leasehold in London for freehold further afield wanes. House instructions also tumbled, but only by 12% – half as much as flats. Those looking for smaller houses (up to 3 bedrooms) would have actually noted more stock this year than Q3 in 2023, while the bigger family homes were fewer and further between this time around, likely attributed to the caution associated with the change of government and some early indications of a taxing Budget in October – pardon the pun.

Sales Agreed

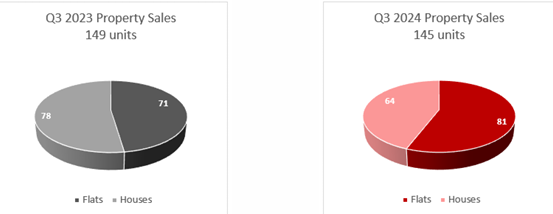

The total number of sales in Q3 of 2024 is almost unchanged from that of the same quarter last year, although flats now make up the majority of these at 56%, compared to 48% in Q3 of last year.

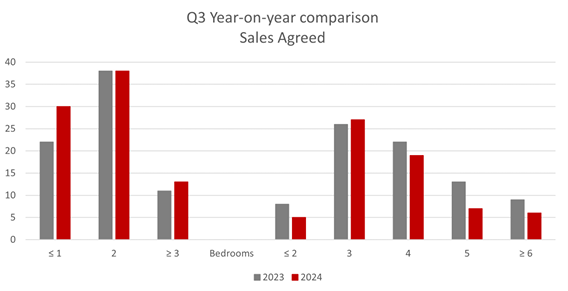

The post-summer period is typically one of the busier periods in the property market for Freehold houses, with families back from holidays and kids back at school. This year, activity picked up as expected for the ‘mass-market’ houses – 3-bedroom house sales nudged up by 1 unit and 4-bedroom house sales correcting by 3 units year-on-year. However, with murmurings of a possible ‘Mansion Tax’ in the upcoming Budget targeting owners of London property valued at or above £2m, and with the average value of the 21 new 5-bedroom houses listed in Q3 of this year sitting at £2,096,429, buyers for the larger houses opted for caution, noted by a year-on-year drop off of 40% in sales of 5+ bedroom houses. That said, house values remained almost unchanged (a slight downwards adjustment of just 0.5%), with just under 24% needing a price reduction to sell in the last three months – a significant improvement on the near 40% of Q3 in 2023. Flats have continued to perform well, with expensive rents, favourable mortgage rates and higher loan-to-value borrowing encouraging first-time-buyer and young-professional demand. Flat values also appear to be heading in the right trajectory, selling for an average £788/sqft in this quarter. This marks a second consecutive year-on-year improvement in flat values, this time of £4/sqft, with 13% less reductions needed year-on-year.

Is that a clear sky I see?

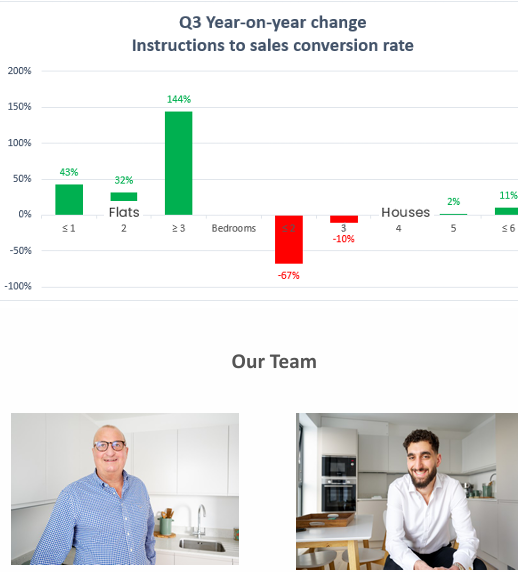

As we enter the final stretch of 2024 and with most economic hurdles now seemingly out the way, the Chiswick property market stands in a strong position - mortgage rates have dropped, inflation has stabilised and, consequently, market confidence has improved. The graph below supports this sentiment, demonstrating that most property types were more likely to sell in Q3 of 2024 than the same period in 2023, including the larger freehold houses! Only ≤2- and 3-bedroom houses slipped on their year-on-year conversion rates, the former to be expected given the small sample sizes and the latter only seeing a slight correction of 10%. 4-bedroom houses remain as popular as ever, shown in the consistent demand-to-supply ratio a year later. After all, Chiswick’s schooling options, transport links and amenities mean the demand for homes in the area will never cease to exist. Overall, the market is showing clear signs of stability and provides much encouragement for the remainder of the year.

Lettings Review Q3 2024

By Katherine McDowall — Lettings, Andrew Nunn & Associates

The fluctuations in supply and demand in Chiswick are significantly influencing the rental market. Some property types are experiencing higher demand and rising rents, others are seeing reduced interest and price adjustments. The overall market appears to be adjusting to these dynamics, with some properties requiring price reductions to secure tenants. The shift in mar ket conditions suggests a transitional phase, where supply and demand imbalances are realigning, with some properties taking longer to let.

Instructions

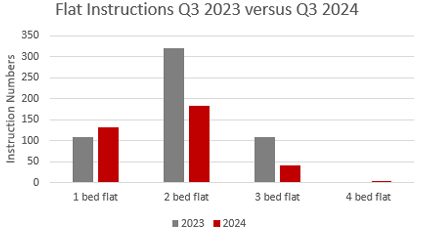

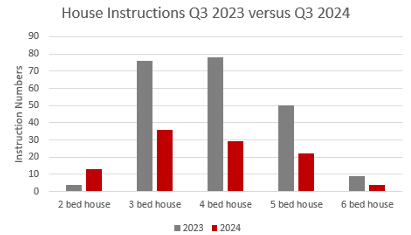

The summer months are traditionally a busier time in lettings and we expected to see more houses coming available during this last quarter. However, overall it appears there is a continual decline in the number of new instructions year-on-year: overall flats are down by 33.7%, while houses are down by 52% versus Q3 2023. A year ago we reported an increase of 7.7% for flats and 66% for houses versus the same quarter in 2022 and so this is a stark difference. One-bedroom flats are the only real exception which have increased by 22.2% (108 - 132) and may be a reflection of tenants moving out to more affordable areas or moving into the ownership market, and two bedroom houses which are not as common to come by thus making this more of an anomaly. Rather surprisingly, two-bedroom flats which tend to be the most popular property type com ing available have substantially decreased by 43.0% (321 - 183), while three-bedroom flats have seen a drop of 63.3% (109 - 40). The 52% reduction in houses coming available are made up of three-bedroom houses which have decreased by 52.6% (76 - 36), four-bedroom houses which have dropped by 62.8% (78 - 29) and five-bedroom houses by 56.0% (50 - 22). The number of six-bedroom houses, although an already low number in 2023, fell from 9 to 4 in 2024, marking a 55.6% decrease. With not so many new houses coming available, it could be argued that most tenants at this level are renewing their existing tenancies as there are not many options for the onward move. A sort of “vicious circle” is emerging? Realistically though the decline in the numbers support the fact that landlords are continuing to sell their investments, likely due to the ongoing challenges with mortgage rates, lender reviews and increased costs on top of the exposure of more risks with the recent change in government and with proposed legislation changes (The Renters (Reform) Act). Additionally, the trend of tenants moving from one- and two-bedroom rental properties into the ownership market may be influenced by the comparative cost benefits of mortgage servicing versus current rent levels.

The summer months are traditionally a busier time in lettings and we expected to see more houses coming available during this last quarter. However, overall it appears there is a continual decline in the number of new instructions year-on-year: overall flats are down by 33.7%, while houses are down by 52% versus Q3 2023. A year ago we reported an increase of 7.7% for flats and 66% for houses versus the same quarter in 2022 and so this is a stark difference. One-bedroom flats are the only real exception which have increased by 22.2% (108 - 132) and may be a reflection of tenants moving out to more affordable areas or moving into the ownership market, and two bedroom houses which are not as common to come by thus making this more of an anomaly. Rather surprisingly, two-bedroom flats which tend to be the most popular property type com ing available have substantially decreased by 43.0% (321 - 183), while three-bedroom flats have seen a drop of 63.3% (109 - 40). The 52% reduction in houses coming available are made up of three-bedroom houses which have decreased by 52.6% (76 - 36), four-bedroom houses which have dropped by 62.8% (78 - 29) and five-bedroom houses by 56.0% (50 - 22). The number of six-bedroom houses, although an already low number in 2023, fell from 9 to 4 in 2024, marking a 55.6% decrease. With not so many new houses coming available, it could be argued that most tenants at this level are renewing their existing tenancies as there are not many options for the onward move. A sort of “vicious circle” is emerging? Realistically though the decline in the numbers support the fact that landlords are continuing to sell their investments, likely due to the ongoing challenges with mortgage rates, lender reviews and increased costs on top of the exposure of more risks with the recent change in government and with proposed legislation changes (The Renters (Reform) Act). Additionally, the trend of tenants moving from one- and two-bedroom rental properties into the ownership market may be influenced by the comparative cost benefits of mortgage servicing versus current rent levels.

Demand

We have observed an increase in applicant registrations, with numbers rising by 12.5% for Q3 2024 versus Q3 2023, which has been a common trend throughout the year. However, with less properties coming available, viewing numbers for Q3 2024 have decreased by 25.6% in comparison to Q3 2023. This decline suggests that while the number of registered applicants have increased, there are less properties which are suitable for them to view due to the shortage of stock. Interestingly though, our collected data shows that it currently takes on average 19 days to let a house and 17 days to let a flat. Comparatively in Q3 2023 it was recorded as 16 days for houses and 11 days for flats, and whilst there isn’t a drastic change in these numbers, it is certainly not the one to two days we saw post pandemic. As properties are taking slightly longer to rent, this extended market time is likely generating more enquiries from a growing pool of applicants. Values Overall average rents for flats in Q3 2024 are approximately 11.6% higher than they were in Q3 2023, with houses up at a more modest but sustainable 1.6%.

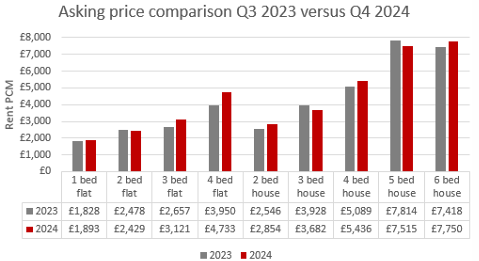

One-bedroom flats have increased by a marginal 3.6% year-on-year, with average rents rising to £1,893 per month from £1,828. Two-bedroom flats have seen a slight decrease of 2.0%, with rents falling to £2,429 from £2,478. Three-bedroom flats have risen significantly by 17.5% with average rents increasing to £3,121 from £2,657, and four-bedroom flats have also seen a notable increase of 19.8% with rents rising to £4,733 from £3,950. The increase in rental values particularly for larger flats, is possibly exaggerated due to lower transaction numbers. In contrast, rental values for houses have shown a mixed pattern. Two-bedroom houses have risen by 12.1%, with average rents increasing to £2,854 from £2,546 although as the number of these instructions have increased significantly, it would suggest there is more competition and boundaries can be pushed. Three-bedroom houses have decreased by 6.3%, with rents falling to £3,682 from £3,928. Four-bedroom houses have experienced an increase of 6.8%, with average rents rising to £5,436 from £5,089. Five-bedroom houses have decreased by 3.8%, with rents falling to £7,515 from £7,814 and six-bedroom houses have increased by 4.5%, with rents rising to £7,750 from £7,418. It is worth noting that in Q3 2024, 21.7% of house instructions required a price reduction to secure a tenant and 33.3% of flat instructions had to be reduced during their marketing period. The year-on-year and quarter-on-quarter statistics indicate an increasing trend in properties needing price reductions, reminding us that rents are not rising as dramatically as they did previously and of a shift in market conditions. Given the contrast between falling instructions and rising values, and with the proposed legislation changes ahead, we anticipate that rents will continue to rise as they have been but more caution will need to be applied when setting those figures.

Yields

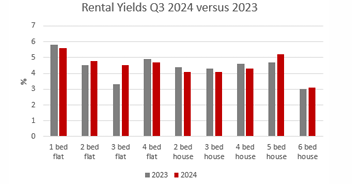

Q3 2024 has seen yields for flats in Chiswick settle at 4.9% and 4.2% for houses. Rental values for flats have increased by some 11% year on year whilst houses have seen a more modest 1.6% increase.

Capital values have risen 1.3% and 1% respectively leading to fairly stable yields. The returns are still not attractive enough to tempt many debt backed investors back into the market but falling mortgage rates and increasing rents may start to redress that balance. Cash rich investors with long term objectives are re-entering the market and cherry picking top quality property which will both perform well in the next growth cycle and also, in the interim, generate strong rental income. For further advice on rental investments please contact Andrew Nunn.

Capital values have risen 1.3% and 1% respectively leading to fairly stable yields. The returns are still not attractive enough to tempt many debt backed investors back into the market but falling mortgage rates and increasing rents may start to redress that balance. Cash rich investors with long term objectives are re-entering the market and cherry picking top quality property which will both perform well in the next growth cycle and also, in the interim, generate strong rental income. For further advice on rental investments please contact Andrew Nunn.

Mortgage Market Review Q3 2024

By James Muncaster — Chagnon Financial Independent Advisors

Mid September brought the welcome signs that Fixed Rate mortgages are falling. We have seen the first 2 year fixed rate under 4% launched since before the fall out of the inflation spikes of the past two and half years. Comparable 2 year fixeds from autumn 2023 were closer to 5%. The psychological difference of a 3.99% rate versus a 4.01% rate cannot be underestimated even if the cost benefit is minimal. Also, it has been encouraging to see 5 year fixed rate mortgages consistently under 4% and falling further. The next step on the path of lower rates is to have a 3.5% 5 year fixed. That would then be a much more relevant con versation in terms of actual value. With markets forward pricing long terms rates around the 3.5% range, a 5yr fixed at this level would seem to be a good long term bet. With the mortgage market being slower in 2023 than first predicted, it seems a lot of the major banks have taken the opportunity to increase lending volumes to finish the year strongly and set up a good start to 2025. With all of them battling for market share, there is a focus on rates to encourage new mortgage customers and this will benefit the consumer. All of the recent improvements in fixed rate mortgages is following the recent Base Rate cut from the Bank of England. The Base Rate was cut to 5% in August. The September meeting, just passed, held rates at 5% with markets forecasting a further rate cut to 4.75% in November. With CPI inflation holding at 2.2% in September and underlying Services inflation and Wage inflation going in the right direction, the inflationary impact seems to be softening. This allows the Bank of England to continue its steady progress to lower rates. As of writing, the next real challenge for the property/mortgage market is the Budget on 30th October. With rumours swirling of tax changes to Inheritance Tax, Capital Gains Tax and possibly Stamp Duty, all eyes will be on what Rachel Reeves announces. Each of these changes, should they happen would impact the property market in some ways. Also, following the Truss/Kwarteng budget of September 2022, the power of the bond market and how this impacts the mortgage market is well known. The politicians also know this, so do now tread carefully around the changes that are made. Let us hope the positivity coming through to end 2024 is not burst by the Budget and we can all look forward to an improving outlook.

* * * * * * * * *