Published: 06/10/2025 By Mateo Asminian & Katherine McDowall

Sales Review Q3 2025By Mateo Asminian — Sales, Andrew Nunn & Associates

The property market in W4 entered the quarter in its typical fashion, with the warm weather and school holidays instigating a summer slowdown, despite the Bank of England’s decision to reduce base rate to 4% in their July meeting. This drop in activity was compounded by rumours of some punitive property tax changes being introduced in the autumn Budget, which we saw the effects of towards the end of the quarter, with September underperforming relative to previous years. However, there were signs of life, with an uptick of buyer enquiries returning in the quarter’s final week, showing some promise for the last three months in the year.

House values increase again Flat sales improve

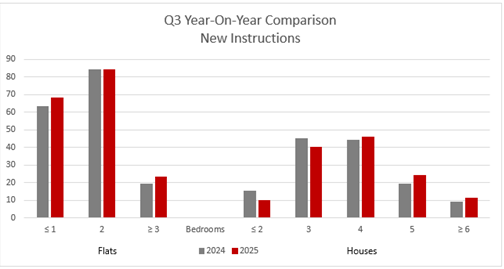

Instructions Stock levels edge upwards House demand weakens

Instructions

New stock levels remained largely unchanged year on year, with flats seeing an increase of just 5% in new listings and the total number of houses coming onto the market in the quarter dropping by just 1 unit. Most notably, we saw more larger houses of 4 or more bedrooms come onto the market in the summer months – a change that many may welcome in an area that is typically short of options in the ‘forever’ home bracket. Flat owners, a not insignificant amount of whom are landlords, continue to face saturated market market conditions, although this trend may begin to die down over the 12 months, once the Renters’ Rights bill has been passed and those landlords who are more inclined to cash in on their investments have done so.

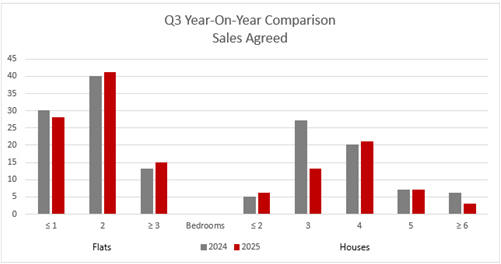

Sales Agreed

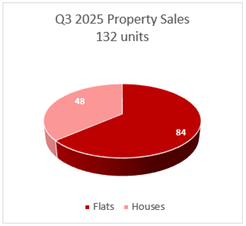

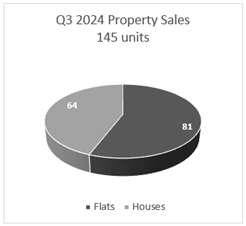

On the surface, the drop in the number of sales agreed of almost 10% in the last 12 months might be perceived as a worrying trend, considering this figure portrays buyer demand and appetite. As ever, however, the devil is in the detail.

One major budget-related headline over the past few months has been the talk of a SDLT reform, with the main rumoured proposal being favourable for those buying at under or around the £500k mark and the opposite for those targeting more expensive properties.

It comes as no surprise, therefore, that smaller, entry level properties – flats – have seen demand grow, albeit by just 4% year on year. This improvement in the volume can also also be attributed to a cooling of 2% (or £18/sqft), while the amount of price reductions needed to sell a flat remained almost equal in Q3, year on year.

It also comes as no surprise that demand for houses plummeted some 25%, as those for whom moving is not a necessity this year hold off until any changes are announced and finances can be reassessed if needed. There remained some activity for houses in the market, with a total of 48 houses successfully going under offer between July and September. What’s more, the amount of reductions needed for houses to sell fell by 24%, while the average value of houses that went under offer in these three months actually improved by 6% year on year, sitting at £906/sqft.

To move or not to move? That is the question... The table below is used to measure how the dynamic between supply and demand has changed compared to the same quarter in the previous year. Evidently, it hasn’t been a straightforward quarter in the property market in W4; however, it’s not all doom and gloom.

Looking ahead, we would expect the caution in the market to remain for the majority of Q4, largely due to the ‘fear of the unknown’ in the budget - all eyes on Rachel Reeves..! Recent history suggests that we should see business as usual thereafter – after all, having suitable accommodation is almost always a non-negotiable. We anticipate demand to rebalance with some slowing of capital growth, leaving little benefit in sellers holding off on their moves. As ever, f you are considering selling and would like to discuss your property and the market, please don’t hesitate to get in touch with us – we’re sure we can add value to your sale.

* * * * * * * * *

Lettings Review Q3 2025

By Katherine McDowall — Lettings, Andrew Nunn & Associates

The Chiswick rental market continues to demonstrate resilience and opportunity. Encouragingly, new flat instructions are up and larger family homes are seeing growth, reflecting sustained confidence among landlords despite broader economic and legislative challenges. Tenant demand remains high, with more applicants registering and viewing properties than this time last year, helping homes still let competitively with rents mostly up year-on-year. Overall, the market shows a healthy balance between supply and demand, presenting a positive outlook for both landlords and tenants.

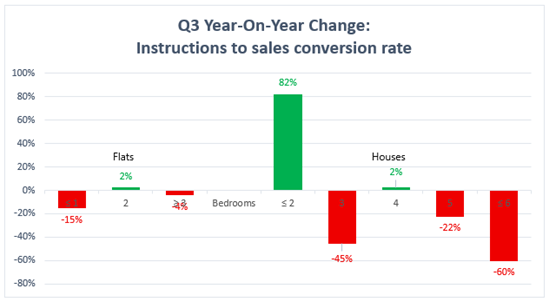

Instructions

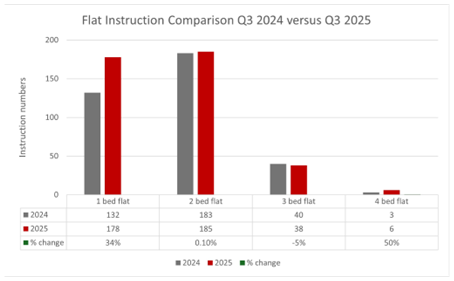

Compared with Q3 2024, the overall number of new flat instructions has risen by 13%, while the supply of houses has remained relatively steady with a modest 7% decline. This is a marked contrast to last year, where both flats and houses recorded sharp annual declines suggesting that, despite wider economic challenges, confidence in the market remains strong. One bedroom flats are up 34%, reflecting ongoing demand for smaller, more affordable properties. Two-bedroom flats, historically the most popular type, have held firm with virtually no change, providing stability at the core of the market. Three bedroom flats saw a slight dip of 5%, but this was offset by an increase in larger four bedroom flats, which doubled year-on year.

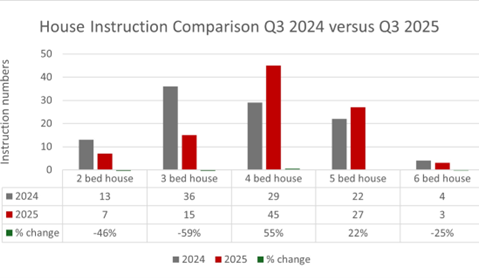

The picture for houses is more varied, though there are notable positives. While smaller two and three bedroom houses are less frequently coming to the market, larger family homes are seeing strong growth. Four bedroom houses rose by 55% and five-bedroom houses by 22%, underlining sustained demand for well-sized properties in Chiswick. Even with a small dip in six bedroom homes, this higher-end segment remains active.

Overall, the figures highlight that the lettings market in Chiswick is far from slowing down – instead it is evolving. Landlords with the right type of property are still finding a keen audience, while tenants continue to see Chiswick as a desirable place to live. For landlords, this evolving landscape presents opportunity. With fewer rental properties overall and strong tenant demand, well-presented homes are letting competitively. While some landlords have chosen to exit the market, those who remain are well-placed to benefit from reduced competition, rising rents in key property types, and continued high demand for Chiswick living. Looking ahead, landlords who adapt and hold their investments are likely to see long-term rewards.

Demand

We continue to witness a significant rise in applicant registrations, which are up by 30% compared to Q3 2024. This growth reflects strong ongoing demand throughout the year. At the same time, viewing numbers have also increased by 42%, proving that more applicants are actively searching for available properties and viewing multiple before making any decisions. As a result, properties continue to take a little longer to let. Currently, it takes an average of 22 days to let a property, just 1 day longer than the last quarter, which suggests this is the new norm. Tenants appear to be weighing their choices carefully, and landlords may need to manage expectations around pricing and ensuring their properties are in the best condition, in order to get the best tenant.

Values

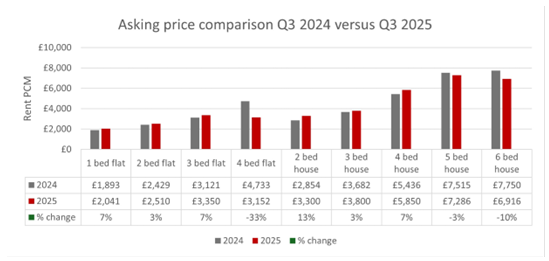

Overall average rents have remained stable year-on-year, with houses showing a small up lift of 0.3%, while flats (at first glance) appear to have dipped by 9%. However, this figure is heavily distorted by the very small number of four bedroom flats coming to market. If we ex clude this anomaly, the picture is much brighter: across one, two and three bedroom flats, average rents have risen strongly, equating to an overall 29% increase. One bedroom flats increased by 7% year-on-year, with average rents now at £2,041pcm compared with £1,893pcm in Q3 2024, which is really quite astonishing. Two bedroom flats rose by 3% to £2,510pcm, while three-bedroom flats also performed well with a 7% increase, reaching £3,350pcm. Four bedroom flats showed a sharp fall of 33%, though with such low transaction volumes, this figure is not representative of the wider market.

Houses have generally held their value or achieved steady growth. Two bedroom houses saw the strongest increase, rising 13% to £3,300pcm, but as we know the numbers will be distorted with the lower instruction numbers coming through. Three bedroom houses followed with a 3% rise to £3,800pcm, while four bedroom houses achieved a solid 7% uplift to £5,850pcm.

At the larger end, five bedroom houses dipped slightly by 3% (£7,286pcm), and six-bedroom houses by 10% (£6,916pcm), though these categories are more sensitive to small changes in supply and seasons. Although the summer months are traditionally the best months for renting houses, a large part of Q3 was the school holidays when it is generally much quieter meaning landlords did on occasion have to adjust their expectations.

Importantly, rental values are holding firm overall, with only 24% of properties requiring a price reduction to secure a tenant, showing that tenants are still willing to pay strong rents where realistic figures are set from the outset. Looking ahead, we expect the market to remain buoyant. With fewer rental instructions overall and continued tenant demand, there is good scope for landlords to achieve competitive rents, provided properties are priced and presented appropriately.

Renters’ Rights Bill

The Bill is in its final stages in Parliament, having been considered by both the House of Commons and the House of Lords. Last month the Government rejected almost all amendments put forward by the House of Lords. In the next ten days they will come back to it and enter what’s called a ‘ping-pong’ stage where the House of Lords will look at the reasons why the House of Commons rejected their amendments and must decide whether to accept their reasonings or seek new amendments. When an agreement is reached, it would be given Royal Assent. This could therefore happen very soon, but the measures will take effect in stages. We are expecting this to become law in late 2025 or early 2026. As soon as this is given Royal Assent we will write to all our clients with the final details of the Bill. If you would like to discuss anything in more detail now, please do not hesitate to contact me.