Published: 11/04/2024 By Mateo Asminian & Katherine McDowall

Sales Review Q4 2023By Mateo Asminian — Sales, Andrew Nunn & Associates

With one of the busiest and one of quietest months in the year falling within the same quarter, it is never clear how the year will end in the property market. October proved to be a slow month by its typical standards, with the Bank of England’s decision not to increase the base rate towards the end of September seemingly encouraging buyers to wait and see what happens next. Their next meeting on 2nd November provided the same outcome, and this consistency appeared to stimulate activity; November’s 30 days alone were responsible for almost half of the quarter’s sales agreed. This late surge carried into the first couple of weeks in December, before the market wound down for the festive period in December.

Total instructions down 25% Total sales up 15% Instructions Slight increase in house values Flat values almost unchanged

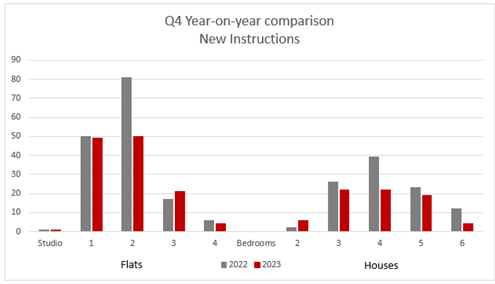

Instructions

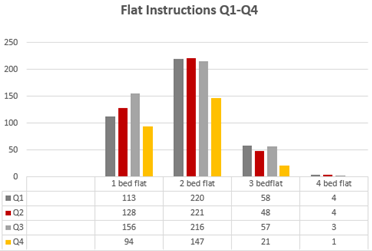

For the fourth straight quarter, W4 stock levels fell when comparing to the same quarter in 2022, down some 25% on the 257 new properties that came onto the market in Q4 2022.

Studio and 1-bedroom flat instructions remained almost unchanged, while 3-bedroom flats were actually up year-on-year levels. It was the 2-bedroom flat bracket that saw the biggest decrease, from the 81 in October, November and December of 2022 to 50 this time around. This comes as no surprise, given the increasing pressure on young professionals (who comprise a large chunk of 2-bedroom flat owners) to ditch their work-from-home habits, and the consequent waning of the ‘size over location’ trend. 4-bedroom flats are already few and far between, and with such a small sample size, it’s no surprise that these were down 50%, reflecting a drop of just two units from the six marketed in Q4 2022.

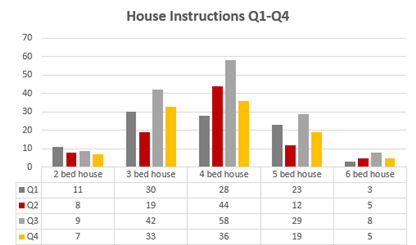

The fall in stock levels was much more consistent for houses, with ‘forever’ homes – 3+- bedroom houses – all taking a hit on their year-on-year comparisons. We attribute this to the flurry of family home sales in the 18 months post lockdown – homes that typically see less turnover over extended periods, and thus less availability following the flurry. The only category of house that exceeded its Q4 2022 levels of stock a year on was the 2-bedroom house; much like bigger flats, these are the vast minority of the total number of houses in W4, and so an uplift of just 4 units year-on-year helped achieve an increase of 200%. These small houses are the most affordable freehold alternative to a flat, and it is no surprise to see more of them coming onto the market, with young professionals more likely to be squeezed by expensive mortgages and rising costs across the board.

Sales Agreed

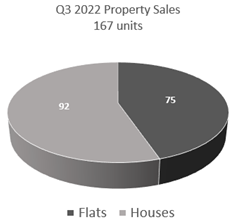

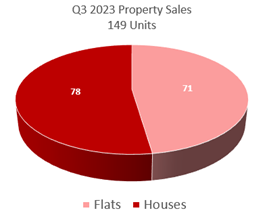

Unlike instructions, property sales in Q4 2023 actually saw a year-on-year increase of 15% on average.

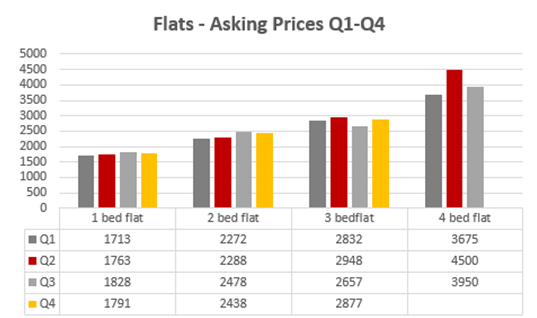

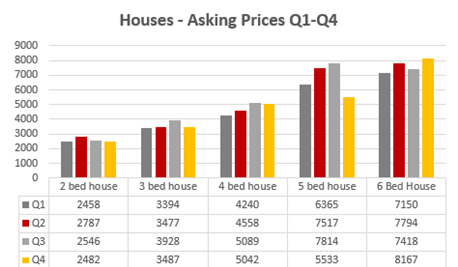

Flat values in Q4 2023 sat at £744/sqft - just over 4% lower than the 7 previous quarters’ average of £776/sqft, and more competitive than in any other quarter since the beginning of 2022. While this data may sound severe, their values in Q4 reflected a ‘trickling down’ of only 0.7% year-on-year. Yet, even a slight correction of pricing appeared to help buyers offset (perhaps more psychologically than materially) inflated mortgage repayments. This, combined with the increasing demand for city living and the growth in rental values over the past 24 months making buying more attractive to tenants undoubtedly contributed to the staggering 32% year-on-year uplift in the number of flat sales generated in this quarter. House sales were some 5% lower in Q4 2023 than the same period in 2022, but the drop in stock of 28.5% had an underpinning effect on values, and even pushed them up marginally in Q4 2023 to £877/sqft from their £865/sqft average in Q4 2022. Of course, Liz Truss’ mini budget in September 2022 did the property market in Q4 no favours, but with base rate 3pp higher in Q4 2022 than a year prior, it is encouraging to see evidence that buyers are adjusting to the ‘new normal’.

So how did the quarter fare?

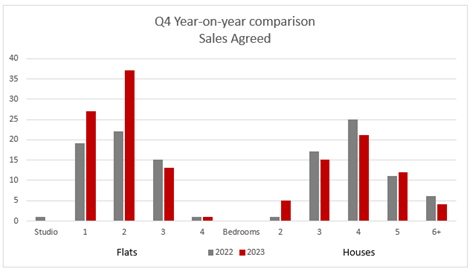

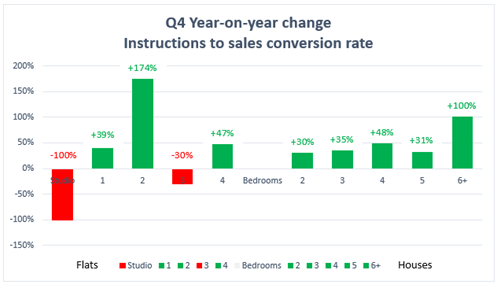

Readers will be pleased to learn that the 2023 market ended very strongly, exceeding the expectations of most. In fact, our data, which we collate and harvest independently, has shown that properties that came on the market towards the end of 2023 were 41.6% more likely to sell than in Q4 of 2022! The graph below shows the year-on-year change in probability of each property type selling in this quarter. The two outermost categories are already low in their instruction and transactional volumes in W4, and hence their figures will be much more volatile, but otherwise the trend is clear and very promising.

And what next?

As we enter 2024, we are likely to have already seen the worst of inflation and rate rises. The mortgage market is becoming increasingly competitive as lenders attempt to improve their market share. An election looms, and it would not be inappropriate to expect some financial inducements introduced that should help stimulate the market in the short term. We anticipate a steady market, with good demand and W4’s typical shortage of stock.

* * * * * * * * *

Lettings Review Q4 2023

By Katherine McDowall - Lettings Andrew Nunn Associates

In summary, whilst the imbalance between demand and supply continued to underpin high rent levels throughout 2023 there was evidence in Q4 to suggest that this dynamic was cooling, that certain properties were taking a little longer to find a tenant and that in 25% of cases a price reduction was required in order to attract the right tenant. That said Q4 is seasonally a quieter quarter and so we will need to wait and see in 2024 whether a trend is emerging or whether Q4 was just a blip.

Instructions

Seasonally and understandably Q4 is historically a weaker quarter for valuations and Instructions as many landlords, over the years, have managed the “availability date” of their tenancies so that the property does not come available in a typically quieter month such as December where there could be more chance of a void period.

The number of house instructions for Q4 were down 31% (100) compared with Q3 (146). Flat instructions were down 40% from 432 to 263.

Our forecast is that there may well be more instructions coming available in 2024, with 2 year tenancies secured during the height of the market in 2022 due to come to an end. During this time when rents were rising rapidly and tenants were struggling to find a property, many wanted to secure a longer term for their protection and these tenancies will be coming to an end during the course of the next year. Tenants will then have the decision to renew or move on, and with rents having cooled a little and more properties available than when they rented last, we’re likely to find some tenants will choose to move on.

Demand

As instructions were lower in Q4, naturally tenant enquiries also dipped over that period however it is worth noting that this has been a trend throughout 2023 in comparison to the extreme levels of demand witnessed throughout 2022. Applicant registrations were down 12% following Q3, with viewing numbers down 40%, neither of which are surprising given the limited choice of new instructions coming to market and seasonal trends. Another factor driving lower viewing numbers towards the end of last year, was that we somewhat struggled to find decent applicants who could meet the required referencing criteria of having a gross income of more than 2.5 times the rent, particularly in the one and two bedroom flat market. For younger professionals, who tend to be on lower incomes, it is now harder for them to rent a small one bedroom apartment at circa £1750pcm or even a room in a house share which could be around £1200pcm whilst in the midst of a cost of living crisis and when rents are higher.

Values

Average rents appeared to marginally fall in Q4 across the majority of property types, however it’s important to stress that rents still remained significantly high compared with those rents achieved prior to the pandemic, and are 55% higher than they were a decade ago.

One and two bedroom flats dropped by 2% and 1% respectively, whilst three, four and five bedroom houses saw seasonal falls of 11%, 1% and 29%. Whilst the flat values changed nominally, house values dipped more significantly due to Q4 being a lean time to rent a house with fewer applicants looking to source accommodation so close to Christmas.

The two property types where rents increased were with the 3 bed flats and 6+ bed houses. 3 bed flats were up 8% with an average rent of £2877pcm in comparison to Q3 and 6+ bed houses were up 10% with an average rent of £8167pcm. However both these property types are traditionally more scarce and so we could see the increases in rent in Q4 as an anomaly due to the smaller sample size rather than a trend.

As demand was lower combined with it taking a little longer to secure a let (on average 12 days for flats and 16 days for houses) we noticed more price reductions. During Q4 we witnessed 23% of flats being reduced, and 25% of houses. Rents were however still strong and higher than we have seen for years.

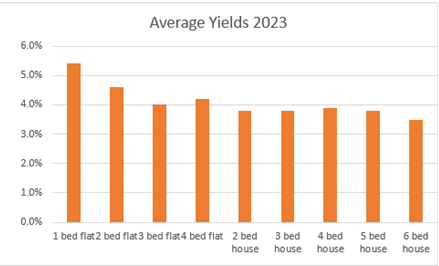

Yields

Whilst the facts contained in this newsletter might seem a little discouraging compared with previous updates, the good news is yields for flat investments increased steadily over the course of 2023.

The average yield for one-bedroom flats stands at 5.5%, as rents continue to rise, and capital values suffer as increased mortgage costs and economic uncertainty hamper the confidence in the sales market. This dynamic also suggests that it could be a good time in 2024 for landlords to come back to the market and replenish their portfolios with a range of smaller units. Yields for houses remained at a rather subdued 3.5%-4% as capital values continued to rise due to a shortage of stock and with buyers willing to take a long-term view.

* * * * * * * * *

2024—The Savings Vs Mortgage Dilemma

By James Muncaster — Director, Chagnon Financial

Following the rate hold on the last Bank of England meeting of 2023, the “money markets” are pricing in an expectation of Base Rate reductions through 2024. This is having a positive impact on fixed rate mortgage pricing. With most banks passing these cuts on but with Base Rate still at 5.25%, the Savings v Mortgage conversation will be relevant in 2024. What I mean by that, is that “Cash” may no longer be King! With the improving fixed rate market and savings rate more tied to Base Rate, putting all your money into a property purchase may not be the most efficient use of the funds. Consider a scenario where you have a mortgage with an annual interest rate of 5%. If the alternative is to invest in a diversified portfolio with an adjusted expected return of 7-9%, the potential gain from investments could outweigh the interest cost of the mortgage and leave you with a better blend of assets, savings & investments. If you have a mortgage of £500,000 with an annual interest cost of £25,000. By maintaining an emergency fund equivalent to three to six months of living expenses (let’s say £15,000), the client ensures financial stability without compromising investment opportunities. The further funds can then be used to create income rather than pay down debt. If the return after costs/tax exceeds the mortgage interest cost, then it’s worth looking at. This also goes along with the Emergency Fund mentioned above, plus being able to exploit investment opportunities, having flexibility in financial planning & some tax efficiency benefits. A simpler route to having the cash flexibility would also be an Offset Mortgage. These products will also become more popular as the rates improve. The ease of having a linked account to the mortgage “offsetting” the balance makes good use of the money, as well. This area is always one that clients get some concern around, due to risk. There is an understandable, psychological need to be debt free on your home but is not always the most prudent use of the funds. It is understandable and rightly so, not to over burden yourself with debt and repayments but striking the right balance could mean a better way of living and not being sat on one asset that is not generating an income even if it is increasing in value. As always the prudent approach is to seek out the right advice from a mortgage broker and/or Financial Advisor to ensure that whatever you decide to buy, you have done so with the right information to hand. With the mortgage rate picture looking much better for 2024, there will be good opportunities out there for property and with the correct mortgage/financial guidance, you could have the best of both worlds.

* * * * * * * * *