Published: 13/01/2025 By Mateo Asminian & Katherine McDowall

Sales Review Q4 2024By Mateo Asminian — Sales, Andrew Nunn & Associates

As we entered Q4 of 2024, with favourable news on inflation and forecasts of rate cuts, activity levels in the property market here in W4 remained strong. In fact, by the time the Budget came around on the 30th October, 41% of the quarter’s sales had already been agreed! The budget announcements appeared to be quite focused on redefining the term “working people,” with the Chancellor opting for a more lenient approach towards property (spare a thought for those buying second homes at this time). The positivity in the property market was compounded a week later when base rate was trimmed for just the second time in over four years, finally dipping back below 5%. Surprisingly, and slightly contrarily, the subsequent 6 weeks saw home supply and demand levels in Chiswick gradually cool, before the market’s second wind kicked in in the last week of December. By the close of the quarter, mortgage rates were some 8% up on average and inflation was back above 2%; however, with buyers and sellers seemingly well-accustomed to these economic blips, sentiment remained positive.

Instructions

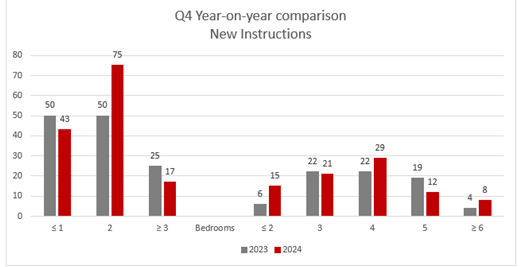

For the third quarter in the year, the number of new instructions coming to market in creased year-on-year, with 22 more listings in Q4 of 2024 than the 198 in the same period in 2023 – an 11% improvement.

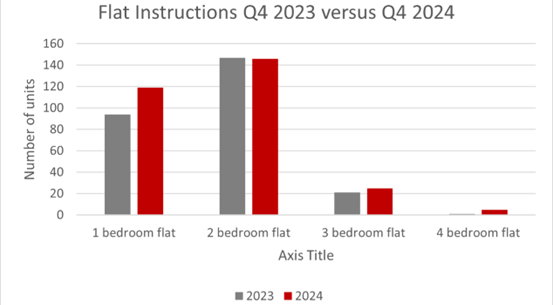

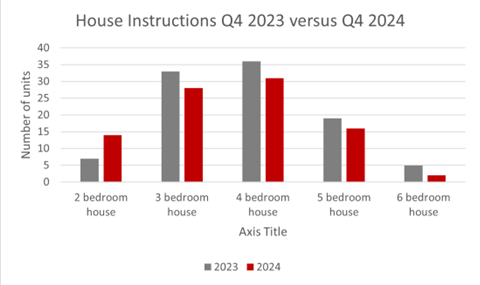

2-bedroom flats saw the most significant increase in stock levels, with 50% more options available in October, November and December of 2024 than within the same three months in 2023. Smaller flats (studio and 1-bedroom) were 7 units down from the 50 of Q4 in the previ ous year and bigger flats (3-or-more bedrooms), an already limited market, were 32% down. Houses on a whole fared well, up 16% (or 12 units) on the 73 that came to market in Q4 of 2023. The only notable change in stock levels among the house categories was in the volume of new instructions for 5-bedroom houses, falling by 7 units – roughly 37%. Otherwise, only 3-bedroom houses saw a dip in stock levels, albeit insignificant (1 unit).

Sales Agreed

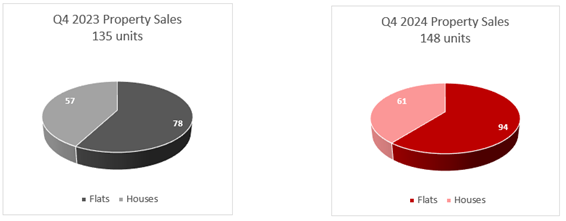

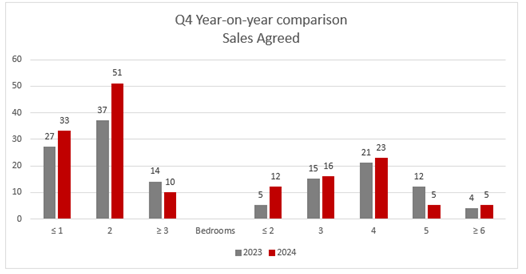

Much like new instructions, the amount of W4 property sold in the final quarter of 2024 in creased when comparing year on year.

In recent years, we have seen the pool of rental properties shrink as increased interest rates, heightened property maintenance costs and also tax changes all trim landlord profits. The shortage of rental stock and the consequent supply and demand imbalance has fuelled well documented rent increases, forcing tenants into reconsidering their living situations and converting a large number of these tenants into buyers instead. With the Chancellor deciding against extending the deadline of 31st March 2025 for first-time buyer stamp duty savings in October’s Budget, the urgency among these buyers intensified. So it is no surprise that the volume of sales of 1 and 2-bedroom flats increased by 22% and 38% year-on-year respectively. Larger flats, of 3 bedrooms or more, had slightly different for tunes, seeing a 29% decrease in volume of sales instead. Houses sales edged up slightly on their year-on-year figures, and it was encouraging to see that all but one category of house saw more sales activity in Q4 of 2024 than that of a year prior.

Optimism going into 2025?

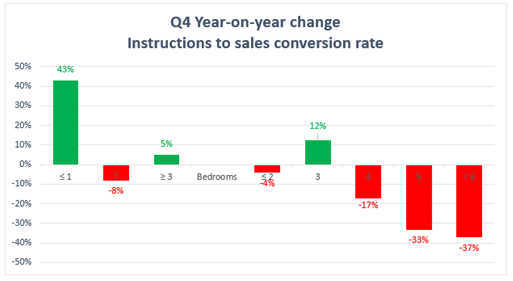

The market in Chiswick showed excellent resilience against the economic and political challenges that emerged in 2024. The conclusion drawn from a quick glance at the graph below, which aims to show the change in likelihood of each property type selling year on year, is that the smaller and more affordable the property, the higher the probability of it selling. Of course, the data only helps paint part of the picture, and with Rightmove reporting that the Christmas period in 2024 produced the most new listings of any Christmas period recorded to date, we would expect the majority of the new listings from the last couple of weeks of 2024 to have sales agreed on them in Q1 of 2025 instead—we may be in for a brisk market in 2025...

Lettings Review Q4 2024

By Katherine McDowall — Lettings, Andrew Nunn & Associates

With the absence of buy to let landlords now firmly impacting on the rental market the inconsistencies of supply have become more exaggerated over the last year and so we are now witnessing more “short term pricing strategies” based on supply levels in the moment. This leads to a market with more optimistic initial pricing but also an increased number of price reductions required before a tenant is found. Year on year rent levels have improved across the board and applicant registrations and viewing numbers in Q4 2024 were very strong suggesting we could expect a buoyant start to 2025.

Instructions

The autumn/winter months often bring a slight slowdown in the lettings market and so we expected to see fewer properties coming to market, but this year has brought some more notable shifts. Overall the total number of instructions are up 6% year-on-year, which is a positive sign as we head into 2025 and following several months of decline in instruction numbers. New flat in structions were up by 12% compared to Q4 2023, whilst houses have continued their down ward trend, with a 9% drop year-on-year. Breaking this down, flat instructions have remained fairly stable with most of these property types seeing an increase year-on-year. One-bedroom flats have seen the most significant in crease, rising by 27% (94 to 119). This may be a reflection of tenants moving into the owner ship market spurred on by marginally more attractive mortgage rates and the stamp duty sav ing deadline of 31st March 2024 but also there are some new build developments in W4 which are likely to have contributed to the increased supply. Four-bedroom flats, though a smaller segment, have shown a 400% increase (1 to 5) while three-bedroom flats have climbed by 19% (21 to 25). However, the market for two-bedroom flats has remained largely stable, with just a 1% decrease (147 to 146). We would have expected the new build developments to have inflated this figure which we are confident it would have done, therefore further highlighting that whilst some new landlords might be coming to market, some existing landlords are exiting.

On the house front, the picture is more subdued. Two-bedroom houses have doubled (7 to 14), but other categories have seen declines: three-bedroom houses are down 15% (33 to 28), four-bedroom houses have decreased by 14% (36 to 31), and five-bedroom houses have dropped 16% (19 to 16).

The numbers continue to reflect ongoing pressures faced by landlords, including high mort gage rates, increased costs, and uncertainty surrounding legislative changes, such as the Renters (Reform) Act. Many landlords are still choosing to sell their investments, further tightening supply. Tenant behaviour will also affect the levels of supply, as with fewer properties coming available, many tenants will choose to stay in their existing rentals than navigate the challenges of moving, and the data shows there are seasonal preferences of when ten ants prefer to move and leading up to Christmas is not usually favoured.

Demand

We have observed an increase in applicant registrations, with numbers rising by 15% for Q4 2024 compared to Q4 2023. This sustained growth reflects strong interest in the rental market, even as landlords and tenants navigate challenging economic conditions. In contrast to previous quarters, viewing numbers have surged by an impressive 72% in Q4 2024 versus Q4 2023. This sharp increase suggests that more properties are drawing interest from prospective tenants, possibly due to a heightened focus on affordability and value, as well as tenants taking advantage of price reductions in the market. Our collected data shows that it currently takes on average 26 days to let a house and 20 days to let a flat. The numbers are slightly up on the same quarter in 2023 which probably reflects the fact applicants have a little more choice and so can take a longer to make a decision.

Values

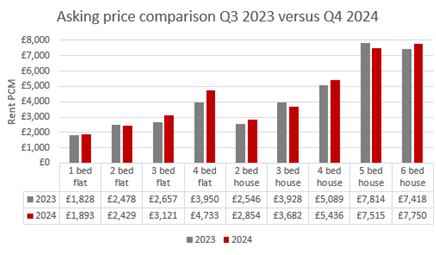

The lettings market in Chiswick has seen an upward trend in rental values in Q4 2024, with overall average rents for flats rising by 14.7% and houses increasing by 14.4% compared to Q4 2023. This increase is reflective of the sustained demand in the area, though it’s important to note that price reductions are becoming more common as landlords adapt to shifting market conditions.

In the flat market, one-bedroom flats have flat lined year-on-year, with average rents rising slightly from £1,791pcm to £1,799pcm. However, rents for 1 bedroom flats had reached an average peak of £1,938pcm (Q3) with the average rents during 2024 sitting around £1,880pcm for the year. When considering this and the fact the Q4 rent figure is just £8 short of the Q4 2023 number, it suggests that Q4 is a less attractive time to rent this property type and that higher rents can be achieved during other times of the year. In contrast, two-bedroom flats have experienced a 7% increase, with rents moving from £2,438pcm to £2,61pcm. Three-bedroom flats have risen more notably by 13%, with rents climbing from £2,877pcm to £3,246pcm, while four-bedroom flats have seen a remarkable increase of 39%, rising from £2,800pcm to £3,899pcm. This increase, particularly for larger f lats, will be somewhat inflated due to lower transaction numbers. Across the board all house types have shown rental growth in Q4 2024, with two-bedroom houses increasing by 19%, from £2,482pcm to £2,959pcm. Meanwhile, three-bedroom houses have risen by a modest 2%, with rents climbing from £3,487pcm to £3,552pcm. Four bedroom houses have experienced a more moderate rise of 3%, with rents moving from £5,042pcm to £5,215pcm. The most significant increases have been in the larger house categories, with five-bedroom houses rising by 19% from £5,533pcm to £6,607pcm, and six bedroom houses increasing by 29%, from £8,167pcm to £10,500pcm. Despite these increases, the market has shown signs of caution, with 44% of house instructions and 34% of flat instructions requiring a price reduction in order to secure a tenant. This indicates that although rents are still on the rise, landlords are having to adjust expectations and be more flexible to meet the current demand, taking into account seasonality, and signal ling a shift towards a more balanced rental market. Tenants are naturally having to be more cautious and if landlords price too aggressively it may cause issues in attracting tenants.

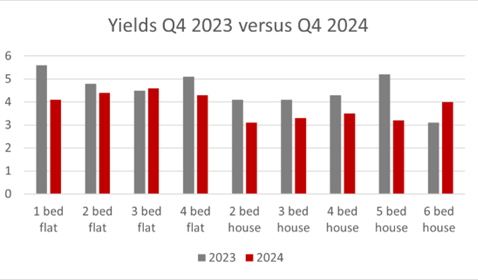

Yields

Yields in Q4 2024 are running at 4.35% for flats and 3.42% for houses which given the high capital values in Chiswick and the current borrowing rates feels about right. The returns are still not attractive enough to tempt many debt backed investors back into the market but cash rich investors with long term objectives are in the market as a hedge against inflation and with the expectation of long term capital growth offsetting the marginally conservative yields.